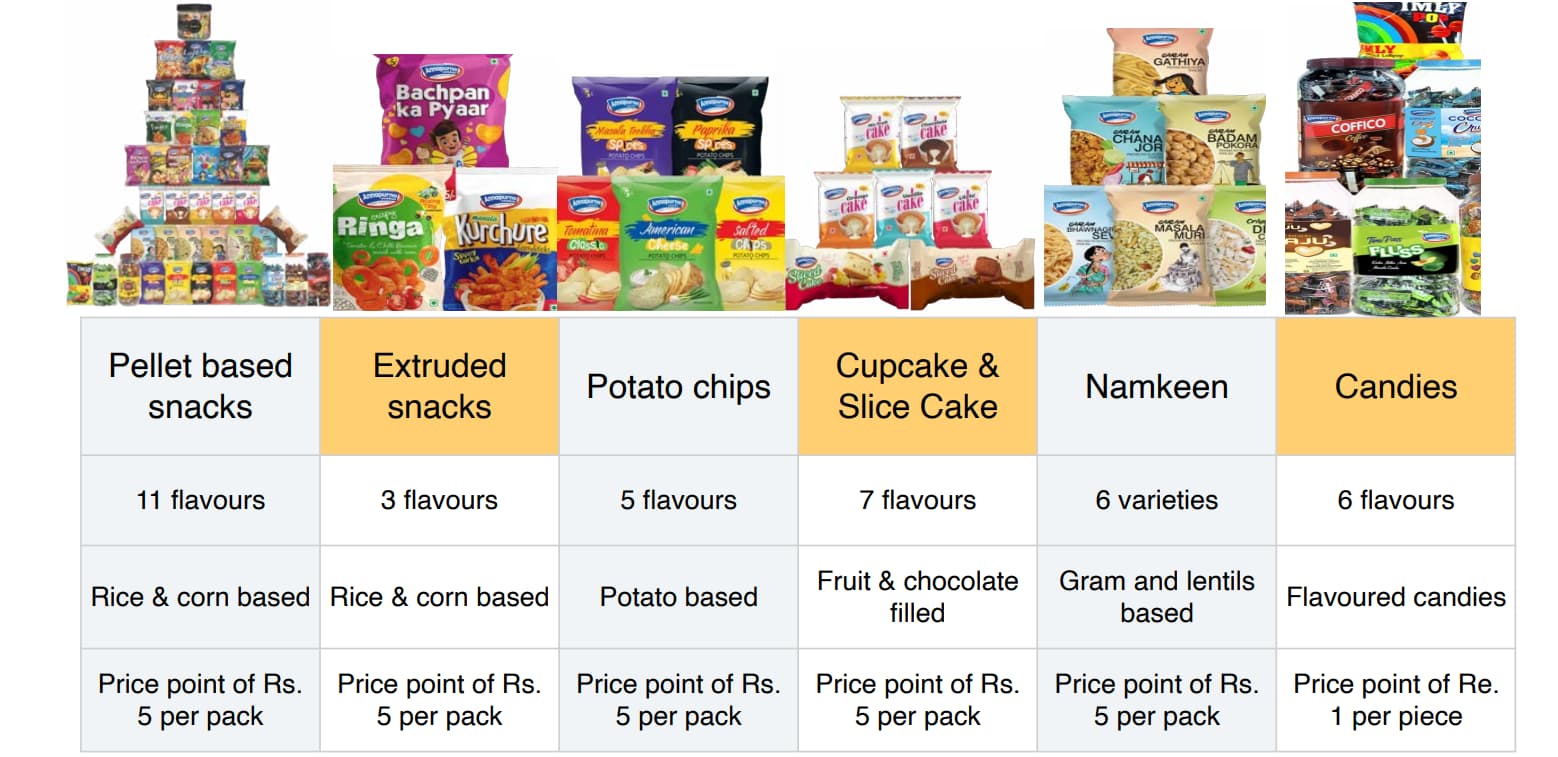

Annapurna Swadisht Limited is a manufacturer of snacks and food products, such as Fryums, cakes, candy, namkeen, chips, and Gohona Bori. The company was incorporated in 2015, and over the years, it has established itself as a brand name in Eastern India. They have a unique price point of Rs. 5, which makes them the dominant player in rural areas.

In FY23, the company enhanced its presence by going beyond the Rs. 5 price point. It forayed into the Rs.10 market with cakes, rusk, and glucose water. Additionally, it entered into the biscuit segment with Rs.30 as the highest product price point.

| PARTICULARS (28-05-2024) | |

| MARKET CAP (Rs in Cr) | 592 |

| PE | 54.6 |

| CMP | 344 |

| ROCE | 23.40% |

| Debt / Eq | 0.37 |

Key numbers that define Annapurna

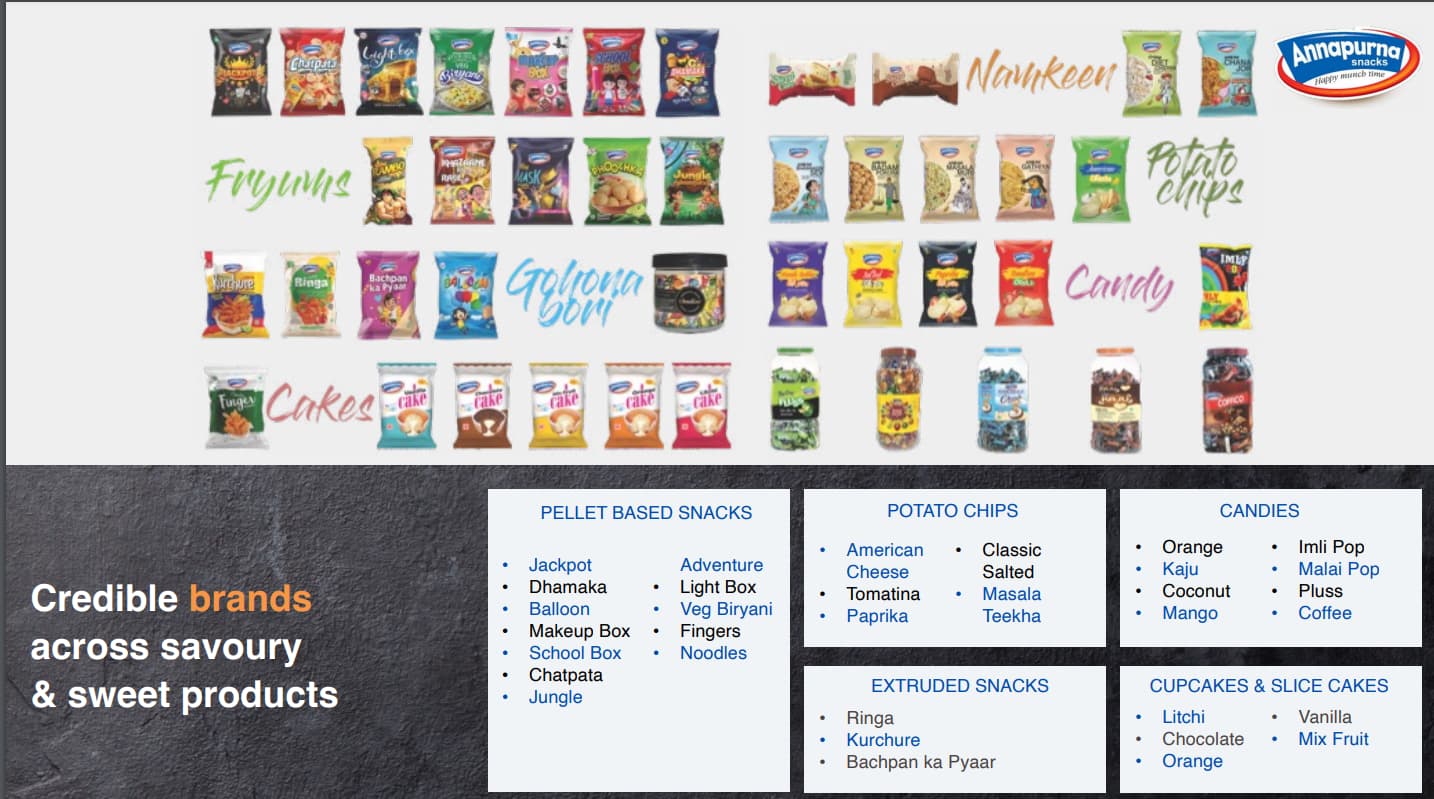

Annapurna Swadisht Limited sells 27 Lakh+ packets of products daily. The company is one of the largest FMCG players in Eastern India in fast-growing segments in Fryums, Cakes, Candies, Namkeen, and Potato Chips.

The company’s products are marketed under its own brand names Jackpot, Chatpata Moon, Balloon, Finger, Rambo, Makeup Box, Dhamaka, Phoochka, Jungle Adventures, Ringa, Bachpan Ka Pyaar, Kurchure, Cream Filled Cake Vanilla, Cream Filled Cake Litchi, among others.

They have been certified by the Food Safety and Standards Authority of India (FSSAI) for quality management systems.

Products and Distribution:

- Currently, they have 75 SKUs across 10 product lines

- 550 plus distributors in West Bengal, Bihar, Odisha, Jharkhand and Assam

- 125 plus Super stockists in key markets (5 states mentioned above)

- 6,00,000 plus retail touchpoints across 250+ towns & 80,000+ villages

Manufacturing Capacity:

Total production capacity of 76 MTPD across four owned units of Annapurna excluding Gurap.

- Asansol

- Area covered: 1,00,000+ sq. ft.

- Areas Catered: Part Of Bengal, Jharkhand, Bihar, Odissa

- Siliguri -1

- Area Covered: 40,000+ sq. ft.

- Areas Catered: Part Of Bengal, NE States, Part Of Bihar

- Siliguri -2

- Area Covered: 40,000+ sq. ft.

- Areas Catered: Part Of Bengal, NE States, Part Of Bihar

- Gurap

- Area Covered: 50,000+ sq. ft.

- Dhulagarh

- Area Covered: 75,000+ sq. ft.

Capacity expansion plans:

Annapurna expects in-house production capacity to increase to 100 MTPD (excluding Gurap)

They have more than doubled their capacities to 70 MT by March 2024. By adding two more manufacturing units in West Bengal (Gurap and Dhulagarh) Annapurna secured backward integration in the Gurap unit with flour mill. Total capex of approx. INR 21 crore+ was laid for the above (Funding mainly from funds raised in IPO).

KEY CONSUMPTION MARKET

Geographical Revenue Breakup (2023-24)

Uttar Pradesh- 8%

West Bengal – 54%

Bihar – 8%

Jharkhand – 14%

Odisha – 2%

Assam – 14%

Financials:

| Particulars | FY20 | FY21 | FY22 | FY23 | FY24TTM |

| Sales | 14 | 20 | 12 | 160 | 226 |

| Expenses | 13 | 19 | 11 | 147 | 204 |

| Operating Profit | 1 | 1 | 1 | 13 | 21 |

| OPM % | 6% | 7% | 8% | 8% | 9% |

| Other Income | 0 | 0 | 0 | 0 | 0 |

| Interest | 0 | 0 | 0 | 2 | 3 |

| Depreciation | 0 | 0 | 0 | 2 | 3 |

| Profit before tax | 1 | 1 | 1 | 10 | 16 |

| Tax % | 34% | 35% | 24% | 28% | |

| Net Profit | 0 | 1 | 1 | 7 | 11 |

| EPS in Rs | 55 | 4.35 | 6.37 |

Annapurna Swadisht Ltd has been growing rapidly in the last 3 years on a lower base. They have grown from a topline of 14cr in FY20 to 226cr in FY24 TTM.

They have grown at a CAGR of 100% from FY20 till FY 2024, which is nothing short of an incredible growth journey!

Annapurna Swadisht Ltd is growing at a phenomenal rate and plans to grow similarly in future (atleast for next couple of years with enhanced capacity).

OPM has increased from 5.5% in 2020 to 9% in 2024. With scale, expect OPM to further improve.

Investment Thesis:

MAJOR GOVERNMENT FOCUS: The government’s focus on bringing back Rural demand can stimulate the growth story of Annapurna.

We believe that the price points of Rs 5 and Rs 10 are a segment where top FMCG giants are failing to meet the demand, and this is where Annapurna has found its niche. Currently, the majority of revenue comes from East India. However, the management is trying to expand its distribution to Northern states such as Uttar Pradesh by setting up a manufacturing capacity in Mathura. This move could significantly boost the company’s growth as it will open doors to states such as Delhi and Haryana, which are considered significant consumers of products manufactured by Annapurna.

They have added new flavours and products to double their SKUs to 76 by March 2024 nearly. They also aim to expand presence across price points to mitigate any potential customer concentration risk.

Annapurna’s plan is to have as much SKUs as possible and have as much as possible products in a shop. They want to fill the smaller shops with their products (Jo dikhta hai wahi bikta hai). In a sense, they are trying to increase their visibility to gain wider acceptance

“Annapurna is a pure play, a scalable and honest management story. The more they can scale, the better their unit economics can get. With management being able to walk the talk, only time will tell how this story plays out in the future.”

Recommendation

BUY

PEER COMPARISON

| Company Name | Price | MCap(Cr) | TTM PE | P/B | ROE(%) | 1 Yr Perform(%) | Net Profit(Rs.) | Net Sales(Rs.) | Debt to Equity |

| Annapurna Swadisht | 336.5 | 591.9 | 54.6 | 9.7 | 11.95 | 33.8 | 7 | 160 | 0.37 |

| Nestle | 2,451.70 | 2,36,382.41 | 73.96 | 83 | 117.71 | 13.6 | 3,932 | 24,393 | 0.01 |

| Britannia | 5,250.55 | 1,26,469.10 | 59.1 | 32 | 54.28 | 14.24 | 2,137 | 16,769 | 0.52 |

| GlaxoSmith Con | 10,753.65 | 45,225.05 | 39.13 | 11 | 24 | 49.03 | 982 | 4,782 | 0 |

| Adani Wilmar | 338.25 | 43,961.63 | 158.06 | 5.3 | 3.36 | -24.9 | 278 | 49,242 | 0.26 |

Risks:

- This is a microcap company is only listed on the NSE SME board. Investing in an SME stock without due diligence can erode your capital quickly.

- At the current market price, the company is trading at 2.68 Market cap to Sales and a P/E of around 55.9, which is not cheap by any means. (We could argue that an FMCG company growing at such a rate could command such valuations).

- Geographical concentration risk: 54% of the revenue was from West Bengal. Need to keep this in mind. (Though management is trying to penetrate Bihar, Jharkhand, Odisha and Assam)

Acquisition:

- a) On March 27th 2024, company entered the edible oil market by acquiring the Arati brand mustard oil from R R Proteins and Agro Ltd (RRPAL) for Rs. 28 Crores, funded partly through internal accruals and partly through debt. RRPAL has a production capacity of 9 lakh liters of oil per month – Annapurna has entered into the edible oil business via acquisition of Arati brand. Hopefully this would also provide backward integration with the consumption of oil manufactured in-house, increasing margins.

- b) On March 19th, 2024, company did an acquisition of 6 acre Plot in Tezpur, Assam, on long-term leases for greenfield projects, to expand its footprint in the North East markets