Arbitrage involves buying and selling the same asset simultaneously across two different markets to profit from the price difference. In the stock markets, arbitrage opportunity exists across the cash (delivery) and the derivative (F&O) market.

In the most basic form delivery positions can be hedged by having a counter position in the futures market**. The big point to note is – inequality of price across markets provides arbitrageurs an opportunity to profit. This price differential is a consequence of the natural process of buying and selling a stock (or its derivative) which may be available for trading on more than one market. Below I will discuss arbitrage opportunity across cash-future and in the option market.

Cash-Future Arbitrage Opportunity

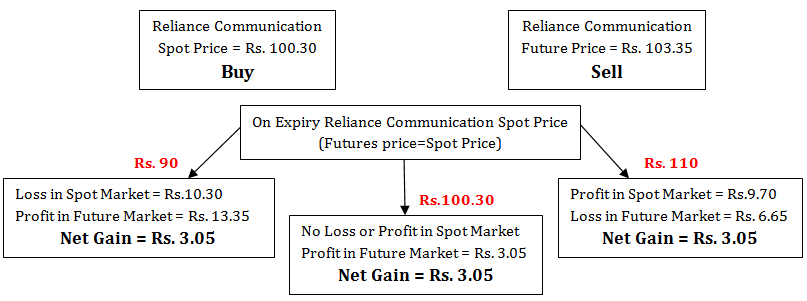

This is best explained with an example. Based on prices on 14th October 2014

Reliance Communications (R-Com) shares are trading at Rs. 100.30 on the NSE, and the near month Futures contract is trading at Rs. 103.35. Arbitrageurs will sell the stock in the futures market and buy an equal quantity of the stock in the cash market to lock in a difference of Rs. 3.05 immediately as profit. As a rule, upon expiry both the futures and cash price of a particular security converges. At this time, they will offset the position i.e. sell R-Com in cash market and buy it in future market. It does not matter what the price of R-Com, may be upon expiry.

Whether the price of R-Com is Rs 60 or Rs. 140 or any other price, the arbitrageur will buy in the future market to settle his short position and will sell his shares in the cash market. In other words, he unwinds both his position. The maximum profit he could make by doing this is Rs. 3.05, i.e. the risk free profit which he made on day one when he entered the arbitrage.

Note: An arbitrageur will not always wait for the expiry of the contract or the settlement of the transaction. They may reverse, i.e. unwind the position and exit before the actual settlement date.

Chart below shows 3 different closing prices on expiry and how the gain is made:

Remember, arbitrage makes sense only if you are able to make a higher profit than what you could make in other risk free opportunities. This is because to do a cash future arbitrage, you will have to block a certain amount which = the amount used in taking delivery of the underlying stock (in cash market) + the amount deposited as margin to take position in the future market. If you take bank FD rate of 8.5% as risk free rate, then for arbitrage to make any sense for you, it should generate a monthly return higher than 0.71% (i.e. 8.5% annualized = 0.70 % on a monthly basis).

Option Market Arbitrage

There are potentially hundreds of arbitrage opportunities in the options market which is why it attracts some of the sharpest minds and gives rise to so much new business activity. The underlying principle in all cases is to profit from the price disparity of option premiums, either across calls and puts of same or different strike prices; or across calls or puts with different strike prices. Here again, unless the return you make is higher than the risk free rate, it is not an attractive option.

Arbitrage Trading – Operational Issues

- Price differentials across different markets usually do not last for more than a few seconds. Trades must be completed within a short span of time otherwise other participants in the market will account for the uneven pricing and correct the market. It is always a race amongst arbitrageurs to discover arbitrage opportunities. For this reason, many arbitrageurs use automated software to find and exploit price differences.

- Future contracts are always traded in lots i.e. one lot of a future contract of a particular stock will have multiple shares in it. For example, one lot of HDFC Bank comprises of 400 shares, while that of Cipla Ltd. has 1000 shares. If an arbitrage opportunity arises in Cipla, you will have to buy 1,000 shares of the company from the cash market and sell one lot of its future contract. Further, if you decide to sell, say, 3 lots, then you need to buy 3,000 shares from the stock market. You need substantial funds to execute arbitrage transactions. Further, you will have to monitor that the price difference i.e. arbitrage opportunity, is not vitiated in the time between you buy and sell in the 2 markets.

Beyond Arbitrage Opportunities

A very popular strategy which I have discussed in our section on option trading strategies is where a long term investor is happy to sell a stock upon achieving a certain strike price. In such a scenario, he could sell (write) call options at that price and profit to the extent of the premium he receives. In case the stock closes above the strike price, his profit will be limited to the premium. Ideally, he would hope that the stock closes just a little below the strike price. Let me explain with an example:

Reliance Industries is trading at Rs. 940 a share. You buy 1000 shares. RIL’s call option expiring 30 October 2014 with a strike price of 960 is trading at Rs. 11.45. You sell 4 lots (RIL lot size – 250 shares) and net Rs. 11,450 (i.e. 250*11.45). If the stock rises above 960, the call buyer will exercise his option and you will have to pay to the extent it rises above Rs. 960. You can sell your stock and pay him J No matter how much it rises, since you have actual delivery position, you will be able to pay him. However, your upside will be capped to a maximum of Rs. 31.45 (Rs. 960 – Rs. 940 + Rs. 11.45).

In case RIL falls from here, you would have reduced your average buy price by Rs. 11.45. You can assume that you purchased 1000 shares for Rs. 927.55. Next month, you can again collect call option premium and basically repeat this until when the stock suddenly jumps in a few days at which time you will have to exit with whatever little profit you make.

** There could be a million ways to earn from an arbitrage opportunity like buying a stock in NSE and selling the same in BSE or vice-versa but cross selling across exchanges in India is not allowed. Still you can earn from such cross market arbitrage opportunities if you find price difference on the two exchanges and you have actual delivery position in the underlying stock, to sell in one market as you buy in the other. This is possible only if you had the underlying stock in your holding from an earlier period of time, i.e. before the day on which you spot the price difference across the 2 exchanges.

I wants to know about algo trading can u help me if possible define about algo trading

I will try and write a post on this soon.

Nice post, Thank you for sharing above information that was really helpful.