I have lost count of the number of queries I have received about the best fixed income investment options. I have refrained from writing about this mostly because I firmly believe that “nobody ever became a millionaire by investing in fixed deposits”.

Yet, people get fascinated by 8% over 7.75%. If you are used to investing in stocks or even mutual funds then there is nothing in it really! Be that as it may, I think everyone should invest some portion of their savings in risk free fixed income investment options.

Nevertheless, after endless suggestions, I finally decided to do a post on this so believe me when I say this. If you don’t find it here – It’s probably not the best when it comes to fixed income investments.

Typically fixed income investments refer to those wherein the amount of cash to be received in future is pre-set and safe. These include government and corporate bonds, saving bank account deposits, corporate deposits, national saving certificates, and Public Provident Fund (PPF).

While bank fixed deposits is by far the most popular investment choice, in the post below I will cover some other options available for urban investors. I will be covering:

- Bank fixed deposits,

- Company deposits and

- Corporate bonds.

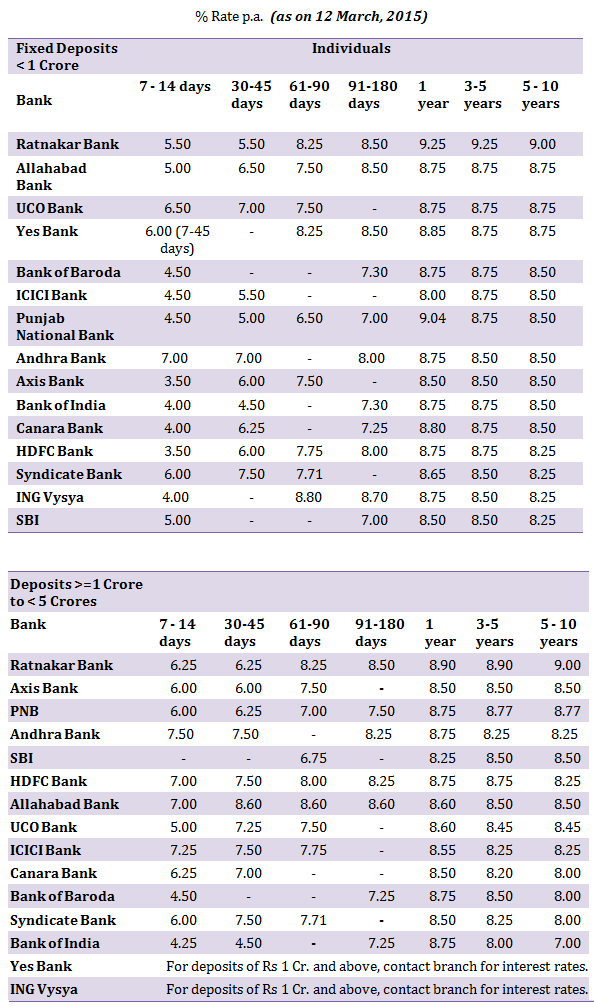

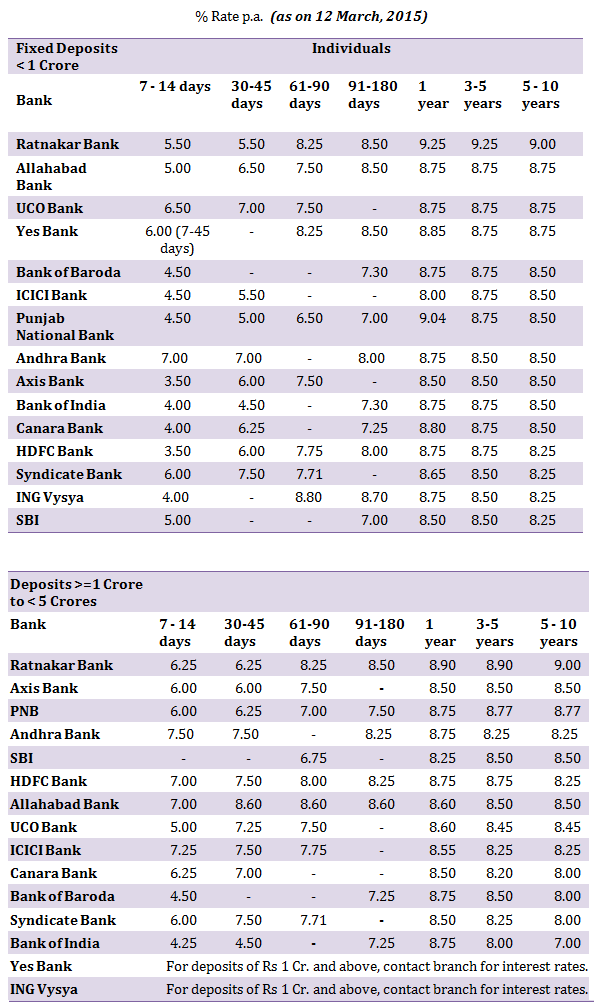

Bank FDs: The biggest benefit is that returns offered by fixed deposits are guaranteed and do not carry market risks. In fact the only risk here is in the very remote possibility of the bank itself becoming bankrupt. Banks give fixed interest returns on deposits ranging from 15 days to 5 years and give you higher interest returns compared to a regular saving account.

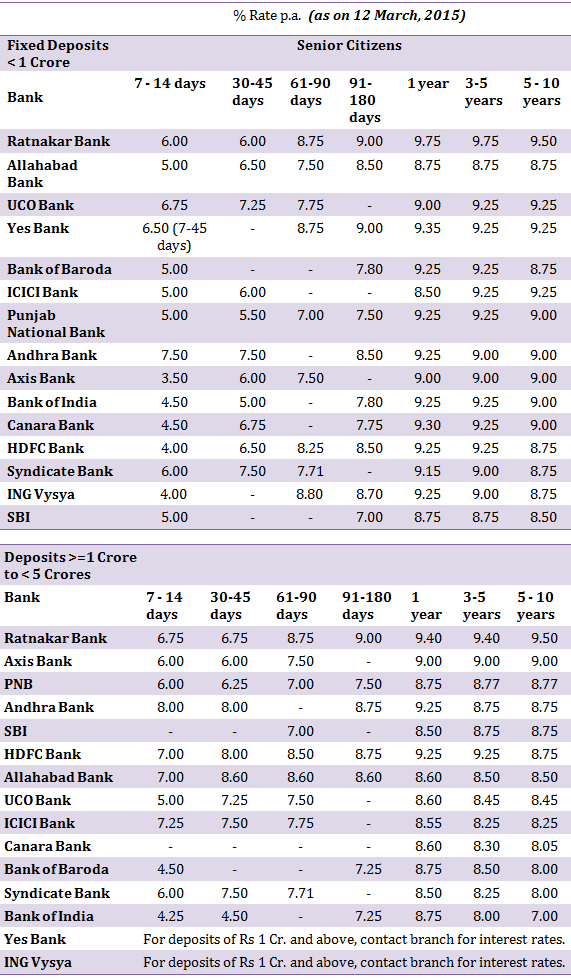

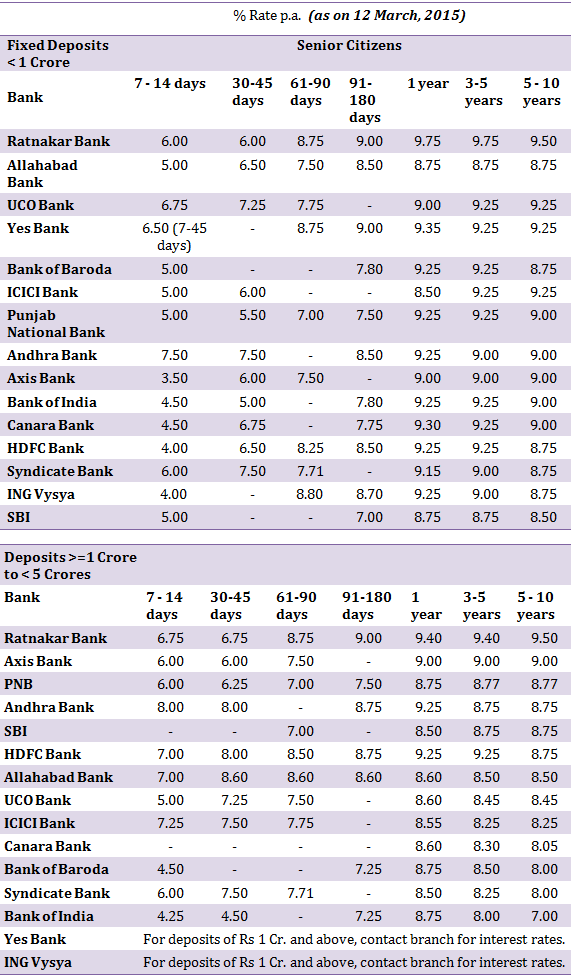

Fixed Deposit Interest Rates Table

3 things to keep in mind:

- Interest Compounding: Most banks use quarterly compounding. You can use the calculator below to check the exact interest payout.

- Most Important – Frequency of interest payouts: How frequently do you wish to receive your interest payouts will have a big bearing on the total interest you receive on your deposits. The reason is simple; your interest component which lies with the bank further earns interest on itself. The difference can be huge based on your principal investment. For example if you make a fixed deposit of Rs. 10,00,000/- @ 8.75% and wish to receive the interest all together upon maturity, the interest payout would be Rs. 90,413. While if you take quarterly payouts, the interest payout for each quarter would be Rs. 21,875. This is Rs. 2913 less over a 12 month period. (i.e. Rs. 21,875*4= Rs. 87,500).

A simple way to do the above math on the calculator above is deposit Rs. 10,00,000 @8.75% compounded quarterl

For 3 month period. Do this 4 times. Its like depositing Rs. 10,00,000 separately at the beginning of each quarter and taking the interest payout at the end of each quarter.

- Size of Principal Amount: On a practical note, the bigger your principal, more you will be able to negotiate the interest rate. While the table above is based on what the banks put out as standard rates on their websites. In practice, if you have a large deposit, you can negotiate with the banks for a higher rate (may be higher by 025-1%). This may also depend upon any other relationships, credit facilities and business which you give to the bank. Keep this in mind.

- Flexi-Deposits: Banks these days sell their savings/ current account products as flexi deposit accounts where your money over a certain limit for example 50,000 automatically starts earning a higher rate of interest i.e. it is treated as a term deposit so long as you maintain that threshold as minimum amount in your account. You may choose any such account to benefit from higher interest rates on your savings accounts.

Company FDs: Deposits in Companies which earn a “fixed rate of return” over a period of time are called Company Fixed Deposits. Financial Institutions and Non-Banking Finance Companies (NBFCs) accept such deposits. These deposits typically offer 1-2% higher rates of interest than bank FDs. The reason: they are riskier since they depend on the well being of the business of the underlying company.

Company FDs are unsecured i.e. not secured by assets. The investors need to be careful in choosing these FDs as lucrative interest rates should not be the only criteria. Even if the returns are lower, it would be better to go with schemes that have a good rating (given by credit research houses like CRISIL, CARE) and a solid track-record.

That said, a smart investor who invests in such corporate FDs will keep an eye on the share price of the company which indicates how well the company is doing. In case the share price starts falling beyond a point, it may well be a good time to sell these bonds before things go from bad to worse. Personally, I see nothing wrong in choosing this option over fixed deposits if you can keep yourself aware of market situation from time to time.

Company Fixed Deposit Interest Rates

| As on 11 March, 2015 | INTEREST ( % ) | |||||

| Company | 1 Year | 2 Year | 3 Year | 5 Year | Additional for Senior Citizens | Minimum Amount |

| GRUH Finance Ltd | 9.00 | 8.75 | 8.50 | 8.25 | 0.25 | 1,000 |

| HUDCO | 9.15 | 9.00 | 9.00 | 8.75 | 0.25 | 10,000 |

| LIC Housing Finance | 8.90 | 9.00 | 9.20 | 9.40 | 0.10 up to Rs. 50,000 and 0.25 for above Rs. 50,000 | 10,000 |

| Mahindra & Mahindra Financial Services | 9.00 | 9.25 | 9.25 | 9.25 | 0.25 | 10,000 |

| PNB Housing Finance Ltd | 9.25 | 9.25 | 9.25 | 9.15 | 0.25 | 20,000 |

| Shriram TransportFinanceUNNATI Scheme | 9.25 | 9.75 | 10.25 | 10.25 | 0.25 | 10,000 |

| SIDBI | 8.75 | 8.50 | 8.50 | 8.25 | 0.50 | 10,000 |

| KTDFC Ltd | 10.00 | 10.00 | 10.00 | 09.75 | 0.25 | 10,000 |

| Bajaj Finance Ltd | 9.25 | 9.40 | 9.65 | 9.25 | 0.25 | 1,50,000 |

| Shriram City Union Finance Ltd | 9.25 | 9.75 | 10.25 | 10.25 | 0.25 | 10,000 |

| National Housing Bank (Suvridhi Scheme) | 8.50 | 0.60 | 10,000 | |||

Corporate bonds/Non Convertible Debentures (NCDs)

These are debt securities issued by public and private companies to supplement their funding requirements. Corporate bonds typically offer higher interest rate in comparison to fixed deposits.

Example of NCDs: In July 2014, Shriram Transport Finance had raised about Rs 3,000 Cr. through a primary issuance of NCDs. The interest coupon offered to individual investors was 10.7-11.5%, depending on the payout option and tenure of the bond.

When the companies issues shares, you become a shareholder and when it issue bonds/NCDs, you become a lender.

Note: Investors should satisfy themselves about the ability of the borrower to repay back the funds at the time of maturity. Senior citizens and conservative investors should choose highly rated and strong institutions.

Company Fixed Deposits (FDs) vs. Non Convertible Debentures (NCDs) – Difference

- Safety:NCDs are secured instruments where lenders can claim if the company fails to repay whereas Company FDs are unsecured and more risky.

- Liquidity:NCDs are traded on exchanges. NCDs give investors the option to sell their units back to the issuer after a specific period. On the other hand, Company FDs are not traded on exchanges.

Find a list of Corporate Bond Listed on the Exchange

Tax Considerations

Interest earned from fixed deposits and corporate bonds and deposits is not tax-free and is taxed as per the an investor’s tax slab. Some banks offer “Tax-saver Fixed Deposit” in which money invested is locked-in for at least 5 years. This is the minimum time-requirement to qualify for the deduction. The maximum amount allowed as deduction is Rs.1.5 lakhs.

The government at times allow some companies to issue tax-free bonds for retail investors.This is mostly when the proceeds are being utilized for some purpose of national interest like building infrastructure (infra-bonds) etc.

Few words on other fixed income options:

- Public Provident Fund (PPF): Public provident funds can be opened with any post office or a bank. PPF investment offers an 8.70 % return, and has a maturity of 15 years. The maximum that can be invested in a year being Rs 1.5 lakh, that counts for tax deduction under 80 (C). Not only the money you invest in PPF is exempt from tax, the interest you earn on the PPF investment is also exempt from tax. IF YOU ARE LOOKING AT YOUR FIRST FIXED INCOME INVESTMENT. THIS IS THE BEST PLACE WHERE YOU SHOULD START INVESTING.

- National Savings Certificates (NSC): National Savings Certificates are issued by the department of Posts and are available at all post office counters in the country and provide an interest rate of 8.5 % for 5 years and 8.8 % for 10 years. The maximum that can be invested in a year is Rs 1 lakh, that counts for tax deduction under 80 (C).