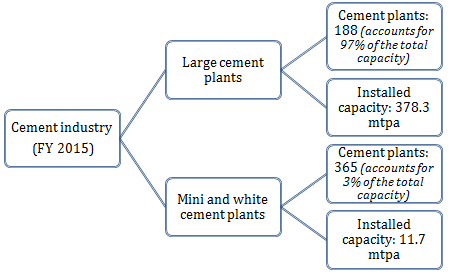

With nearly 390 million tonnes of cement production capacity, India is the second largest cement producer in the world (after China) accounting for about 8 % of the total global cement production. Large cement plants account for 97% of the total installed capacity in India. By 2020, cement production in India will reach 550 million tonnes.

Cement Industry – Demand Driver

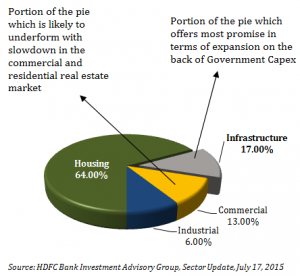

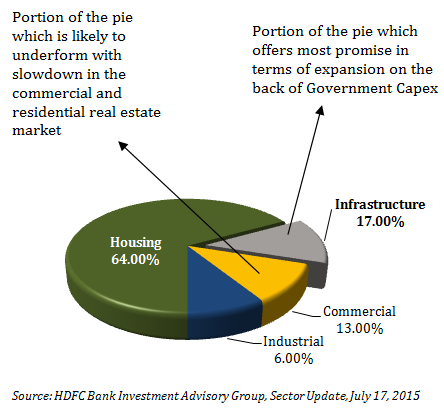

Housing industry is the biggest consumer of cement, accounting for about 64% of the total cement consumption, followed by infrastructure (17%), commercial construction (13%) and industrial construction (6%).

View

While demand from the housing industry is declining with new house construction activity slowing down due to a current oversupply, cement demand in coming years is likely to improve from increased government spending on infrastructure. At current prices the entire cement pack looks expensive. Cement stocks rallied towards the middle of last year after the new government took office with expectation of increased infrastructure activity. However, earnings (EPS) have not improved in line with expectation.

Going forward, focus on companies with greater presence in southern Indian states where bulk of new infrastructure projects will be developed. These companies will get logistical advantage given their proximity to these upcoming projects.

Some of the Big Upcoming/Under Construction Infrastructure Projects

- South – Infrastructure project initiated by the Andhra Pradesh government – Amravati project. According to Andhra Pradesh’s government, approximately 2 million tonnes of cement will be required annually for this project.

- South – Rs. 5,000 Cr. Mega Transhipment Hub Project in Tamil Nadu.

- South – Rs. 14,000 Cr. 72-km elevated metro project in Telangana.

- North – Rs 80,000 Cr. Bharat Mala project (7,000 kms) connecting Gujarat, Rajasthan, Punjab, J&K, HP, Uttarakhand, part of UP, Bihar and West Bengal.

- North – Rs. 12,000 Cr. project (889 km) connecting Char Dham (Kedarnath, Badrinath, Gangotri and Yamunotri in Uttarakhand).

- West – Rs 90,000-crore Mumbai-Ahmedabad bullet train project.

- Pan India – Four major industrial corridor development projects – Delhi-Mumbai, Amritsar-Kolkata, Vizag-Chennai and Bangalore-Mumbai.

Top 10 Cement Stocks in India (by Market Cap as on 21 December, 2015)

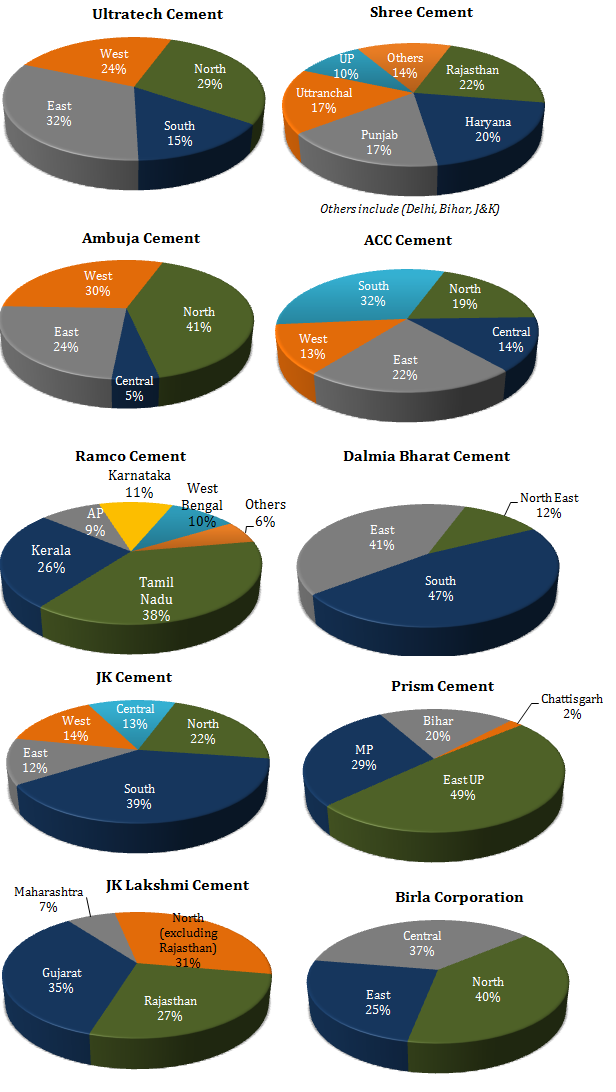

Cement Stocks : Geographical Split (by Revenue)

Also see : Cement Stocks in India – Industry Insight

| Revenue | Net profit | Debt – Equity Ratio | Interest Coverage Ratio | |

| UltraTech | 24,349 | 2,098 | 0.26 | 7.54 |

| Shree | 6,454 | 462 | 0.08 | 11.11 |

| Ambuja | 10,000 | 1,487 | 0.00 | 29.21 |

| ACC | 11,739 | 1,162 | 0.00 | 18.23 |

| Ramco | 3,655 | 246 | 0.87 | 3.69 |

| Dalmia Bharat | 3,514 | 3 | 2.08 | 1.39 |

| J. K. Cement | 3,399 | 144 | 1.86 | 1.93 |

| Prism Cement | 5,654 | 3 | 1.88 | 1.21 |

| JK Lakshmi Cement | 2,316 | 103 | 1.27 | 3.76 |

| Birla Corp | 3,210 | 175 | 0.47 | 3.87 |

Regionalization

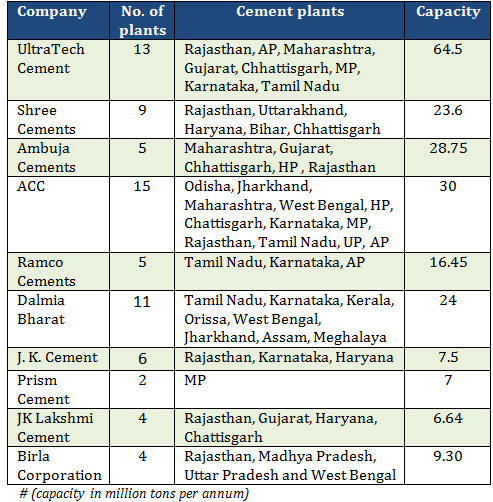

Cement is a freight-intensive industry. Transport over long distances is a big problem for the cement companies. This has made cement industry largely a regional play. While deciding on the plant location, there is a trade-off between proximity to raw material sources and proximity to markets/projects. Ultratech, ACC and Ambuja will likely to benefit from the proposed boost to infrastructure projects due to their pan-India presence.

Pan India Presence

- UltraTech Cement

- Ambuja Cements

- ACC

North

- Shree Cements

- JK Lakshmi Cement

- K. Cement

- Birla Corporation

South

- Ramco Cements

- Dalmia Bharat

Central

- Prism Cement

Geographical Presence (by Capacity)

good information sharing

Thanks, Rajat, great info.

I think Ambuja is the best among these stocks.

Right?

From my perspective they are all over valued for now.

What’s your thoughts on Deccan Cements?

Why does Shree cement enjoys higher valuation (P/E – 83X ) compared to Ambuja, ACC & others even though the Avg ROE, D/E are comparable.

Thank you so much, very use full information. ACC and Ramco looks good for 2016