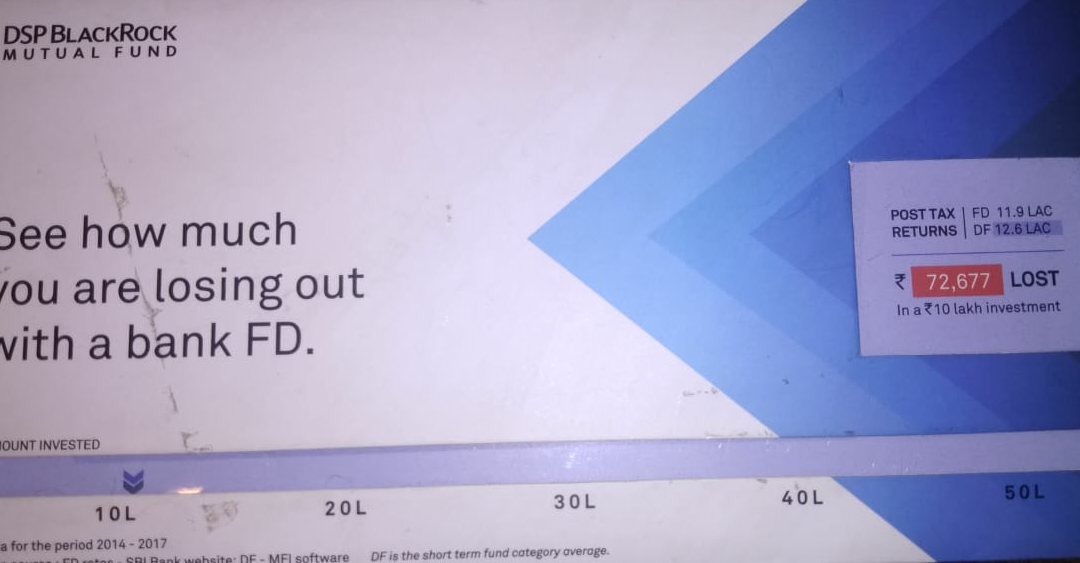

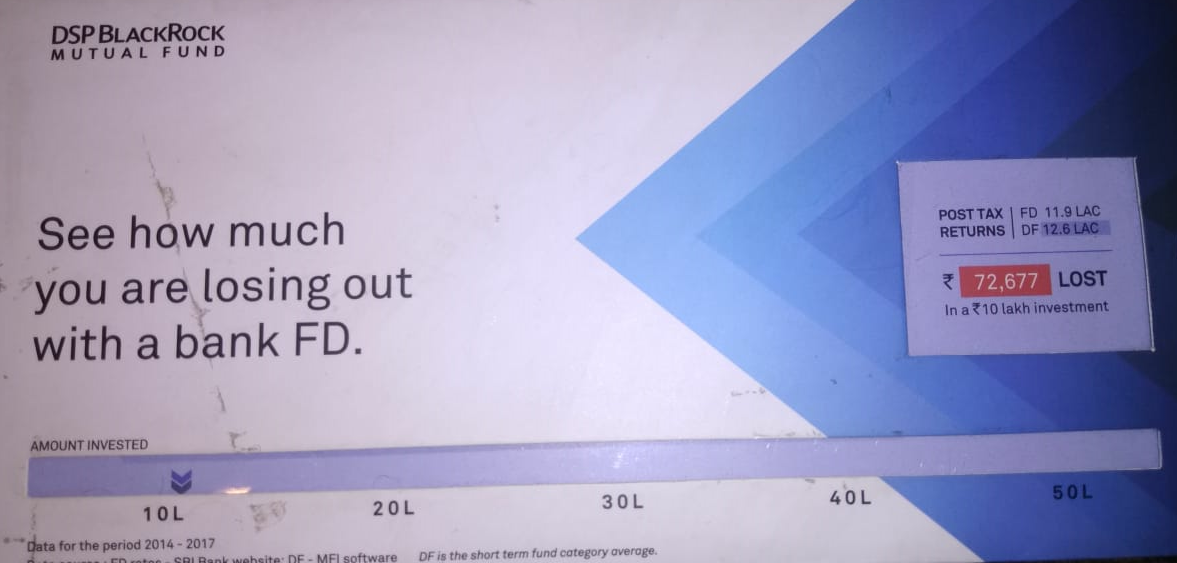

Over the last few years debt mutual funds have gained popularity over fixed deposits, purportedly for tax efficiency and better returns. The real reason for their popularity however lies in the fact that these funds were promoted far more aggresively than other fixed income products like fixed deposits. This, even if listed securities by their very nature can hardly ever offer a fixed rate of return. Here’s some marketing which pushed for Debt funds as better than FD instruments.

In many cases this was just marketing while in others – lack of understanding of the product.

Are debt funds a bad product?

No

Can they be replacement for FD/ Fixed income products.

Again – No.

The Problem

Quite simply, mutual fund houses started doing what was traditionally a banks job – to extend loans to corporates. The banking system came under severe stress because of rising NPAs and hence could not extend as much credit as was needed. Mutual fund houses and NBFCs started filling in this gap by extending capital to corporates with reasonable and in some cases below reasonable credit rating. Corporates in turn started tapping into this market as the size of the mutual fund industry expanded. As more and more investors started investing in mutual funds, fund managers were faced with the hard task of looking for newer investment avenues. As a result, many inferior quality credit papers were issued and were quickly endorsed by fund managers.

NBFCs are already feeling liquidity crunch with many depositors and backers redeeming their investments.

A bigger fear in fact remains that many more companies which issued these credit papers may default. Think about it – Banks which have a higher diligence standard could not extend loans; in turn, fund houses with a much lower compliance standard are now doing this job. How do you think this will end?

I have consistently warned investors against blindly investing in debt mutual funds and still believe that to counter stock market volatility, debt funds are not the best investment option and should definitely not be confused with a fixed income prioduct like an FD. Here’s some past evidence to this effect:

1 Year returns of some top Debt Mutual Funds of past (rankings have of course changed)

| Mutual Fund Scheme | 1 mth | 3 mth | 6 mth | 1 yr |

| Tata Short Term Bond Fund – Regular (G) | 0.60 | 2.50 | (2.30) | 0.20 |

| ABSL Medium Term Plan – RP (G) | (1.10) | 0.60 | 0.90 | 4.00 |

| DHFL Pramerica Medium Term Fund(G) | (0.50) | 1.60 | 2.20 | 4.10 |

| UTI Bond Fund (G) | (2.00) | (0.70) | (0.10) | 1.90 |

| ABSL Dynamic Bond – D (G) | (0.40) | 2.30 | 3.80 | 6.30 |

| Baroda Pioneer Dyn Bond -Direct (G) | (0.70) | 2.30 | 4.30 | 6.40 |

| UTI Dynamic Bond Fund – Direct (G) | (2.00) | (0.30) | 0.70 | 3.50 |

| HDFC Dynamic Debt Fund – D (G) | (2.00) | 0.20 | 1.30 | 2.90 |

| Franklin (I) Govt Sec -CP (G) | (0.10) | 0.90 | (3.80) | (3.30) |

| Edelweiss Corporate Bond Fund (G) | (0.10) | 2.30 | 2.20 | 4.30 |

| DSP Credit Risk – DP (G) | 0.80 | (2.00) | (4.30) | (1.60) |

| Invesco India Credit Risk – D (G) | (6.40) | (4.50) | (5.40) | (2.30) |

| Motilal Ultra Short Term – (G) | 0.60 | (6.20) | (10.80) | (7.90) |

| Tata Money Market Fund – D (G) | 0.90 | 2.70 | (3.30) | 0.40 |

Over the past 1 year, an investor would have made 1-2% less in the best of debt category fund when compared to a fixed deposit. At worst, his return could be a high single digit negative. Assuming even if this underperformance is corrected in future as your advisor may say (i.e. that debt funds deliever in excess of 8-9% over the next 2-3 years), it would take more than 5 years to generate as much return as a traditional fixed deposit would have generated if investment was made in an FD. In any event, I doubt that any significant outperformance will be witnessed in a majority of debt category funds.

There are better products to earn a fixed 9 – 10% p.a. interet with absolute certainty. Avoid the lure of marketing and invest sensibly.