A man once discovered a large treasure consisting of an unquantifiable amount of gold and diamonds buried under his house. He started digging and realized that at some point the entire treasure will come out of the earth. To make most of the situation and the frenzy created by his discovery he decided to invite people to share his treasure. The story he came up with was as exciting as the discovery –

“I got gold under my house! Proven, unlimited reserves. I cannot dig it all out on my own. Help me dig it out and in return I will give you 50% of what you dig. If you agree, send an amount of Rs. 624 ASAP to receive your entry pass to the house. Digging starts in 8 days from now”.

Over the next 8 days he did 2 things:

- Dug out up to the last ounce of gold from the earth.

- Collected over 54,000 subscriptions of Rs. 624 each from prospective diggers.

8 days later he gave an axe to each of the 54,000 people before starting a new life on a beautiful island in Bora Bora.

_____________________

About Money Raising: Need for Money vs. Unlocking Value vs. Promoters / Investors Exiting

Why exactly do companies raise money? I had written a detailed piece on this – Investing in IPO’s where I discussed why companies do IPOs in some detail. Broadly these reasons fall under one of the three categories – (i) genuine need for cash to scale up the business, (ii) to unlock value, (getting listed on an exchange is a great way of discovering the true value of a business, i.e. a something is only worth what someone is willing to pay for it), and (iii) to allow private equity / promoters or other existing investors to exit from the business.

This third and final reason is perhaps the most common one when it comes to E-commerce companies. Take Flipkart for example – a lot of private equity money has been invested in this venture. But why would investors or promoters want to sell their stake now that the business is a runaway success?

Those who invest in a new business (i.e. start up) would naturally want to recover their initial investment with a certain rate of return or profit. On the other hand, those who buy such businesses at a later stage would normally not make those kinds of returns because the risk involved in a well established and running business is far lesser compared to a start up.

Think of it this way – for IPO investors, the level of risk is more than what it is for fixed incomes investors (like a bank fixed deposit which pays 7.5% p.a. interest) but far less than it is in case of investing in a startup. Secondly, private equity investors could make a killing by offloading stake in businesses that does well and one in which they had invested seed capital. At the same time PE investors invest in many start-up businesses which fail. Their success depends on how many successful businesses they can spot at an early stage.

But – If their investment in this business will keep giving them a rate of return far higher than the fixed income rate, why not stay invested?

– Mostly because they are looking for a far higher rate of return and are willing to assume a far greater risk. That is the very nature of their business.

Other investors who buy post the company achieving a certain degree of success will naturally not get the ‘historic success premium’,but again, their goals are different. They may want to make a rate higher than the fixed income rate (~ 7.5 % – bank rate), or may believe that the company can still generate outstanding profits going forward, may be little less or more that it’s historic trends. In general however, they are not willing to assume the kind of risk which PE funds take on.

That said; think about it – “You are planning to buy something which insiders (those who know more about the business than you) are planning to sell?”

E-commerce Companies – Will you buy into the buzz?

I am confident that over the next 4-6 years as the primary equity markets revive, dealing officers at SEBI will be handling a lot of new paper and if the market sentiment is anything to go buy, it is all likely to be absorbed.

Existing E-Commerce companies in India

Over the last few months, I have had many prospective investors asking for investment opportunities in the E-commerce space. I have studied laws (in the United States) which prohibit conditioning the market before an issue to prop-up the demand for the shares to be listed under the issue. I am not sure if such frenzy was initiated by the companies or their financial advisors (i.e. investment banks) but there is no doubt in my mind that these companies will get attractive valuations when they hit the market:

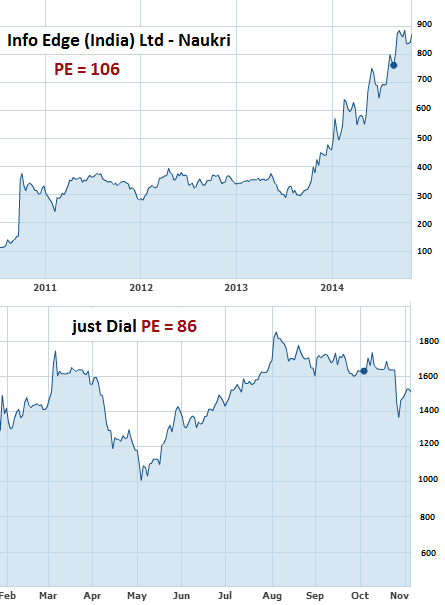

Valuations for the existing E-commerce companies in India:

The story in the west is no different. Inface e-commerce stocks are rallying despite reporting negative EPS (technically – an infinite PE multiple). A global buzz if you may.

How I would go about valuing these businesses

If the owners of Flipkart were to offer equity in their business, in other words, if they were to tell me “we are done with owning this business or at least the whole of it, why don’t you own some of it” what will I do?

My basis of evaluating such a proposal would remain the same as it will be for any other business:

-

Valuations – On what terms

-

Future plans – What do you plan to do with the money you raise?

Now frankly I have never understood the basis of valuing companies which do not have a readily available industry PE (that said, the ones that have are equally difficult to value). The best way to do this is not to buy into the IPO at all. Let the big investors with their big diligence teams lead the way. Anyways they have a bigger appetite for speculative investment. In addition, you save your money getting blocked and filling up ASBA forms. Just let the damn thing list and buy from open market. Of course this is the easy way. If you really must discuss valuations, feel free to call me when the next e-commerce company gets on its way.

The perfect case in point to support my argument is Facebook. The stock declined by over 50% within 2 months from its listing. Currently 30 months on from its listing it is trading 100% higher from its listing price. Facebook listed on the Nasdaq on 13 May 2012 @ US$ 38.23 a share, made a low of US$ 18.06 on 26 August 26 2012 and is currently trading at US$ 76.

Before I forget to mention this – E-commerce companies are at the higher end of the quick boom and bust cycle of the overall IT space. They could show phenomenol growth in a fairly quick time as their business catches the frenzy of people at large but is equally likely to perish rather quickly once a better website with better functionality comes along. Those who remember the dot com bubble of the late 90’s – early 2000’s would probably relate better to what I am saying.

As for ‘Use of Proceeds’

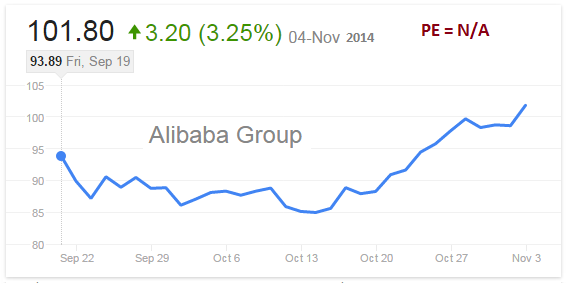

Here is one example of a company I will hesitate from buying into, even though it has had a super listing.

Alibaba.com’s stated use of IPO proceeds:

“We plan to use the net proceeds we will receive from this offering for general corporate purposes.”

It’s like saying – we have a running business, judge it yourself. Your money will go into what we do. You will get a rate of return similar based on our past rate of profits. It’s like a bank fixed deposit with a high rate of return; we call it the alibaba deposit.

Check the offer document and check if the company has better plans than this. That said, I am not criticizing alibaba at all. If you believe that E-commerce companies will keep growing and you will keep gaining from bigger market shares do go ahead and buy but even then ask yourself this – if there is no particular need for the proceeds and the business will keep profiting, why are these guys selling the business to me?

Dear Rajat_Ji,

Two things make the basic difference in life. One is knowledge and other is WISDOM. Your approach is excellent. Wisdom should alwasys outweigh the knowledge. Your approach is perfect. For an ordinary investor, whatever knowledge or skill he or she might possess for valuation of companies under such situation, it can never be sufficient. So wisdom should prevail. Moreover first lesson of technical analysis says market price discounts everything.

Excellent post

Thanks Ratnadwip – I am not a technicals person but I like what you say at the end – ‘Market price discounts everything’, its a hard lesson to learn at times.