Over the past few years, The Reserve Bank of India (RBI) has consistently lowered interest rates. Consider this, The RBI has lowered its Repo Rate (i.e. the rate at which RBI lends to commercial banks) from a high of 8% in 2015 to its current rate of 4%.

Falling interest rates have resulted in a significant reduction in Fixed Deposit (FD) returns. If you compare the current rate of interest on bank FDs with current rate of inflation (of ~ 6%), you will recognize the importance of other tax efficient instruments like debt funds, which can potentially generate a higher return and are far more tax efficient than a bank FD. That being said, investors should understand how and which category of debt fund should be used for wealth preservation.

A good debt fund is one which aligns with your goal of earning a higher and tax efficient rate of return, while ensuring safety of principal . How then should you choose the correct category of debt fund when your goal is to preserve long term wealth which grows at a rate higher than FD?

How to choose the right Debt Mutual Fund to replace FD

Unlike an FD, a debt fund needs a lot more study of the paper quality and tenure for which it invests.

There are debt funds, which are in fact safer than FDs and offer better returns than FDs. At the same time there are debt funds which carry a far higher risk than FDs but offer a much better risk adjusted return.

The key to selecting an appropriate fund has much to do with where the fund invests. In the current economic scenario, credit risk funds and corporate funds naturally carry a higher risk (but higher reward potential) compared to Government security funds (Also Read: “What’s a good FD Replacement”, at the end)

Whether you like it or not, debt funds are not FD replacements. The return generated by a debt fund is not linear. It can be volatile based on changing interest rates and quality of paper.

I have covered this point in greater detail here – Which Debt Mutual Fund Should You Buy?

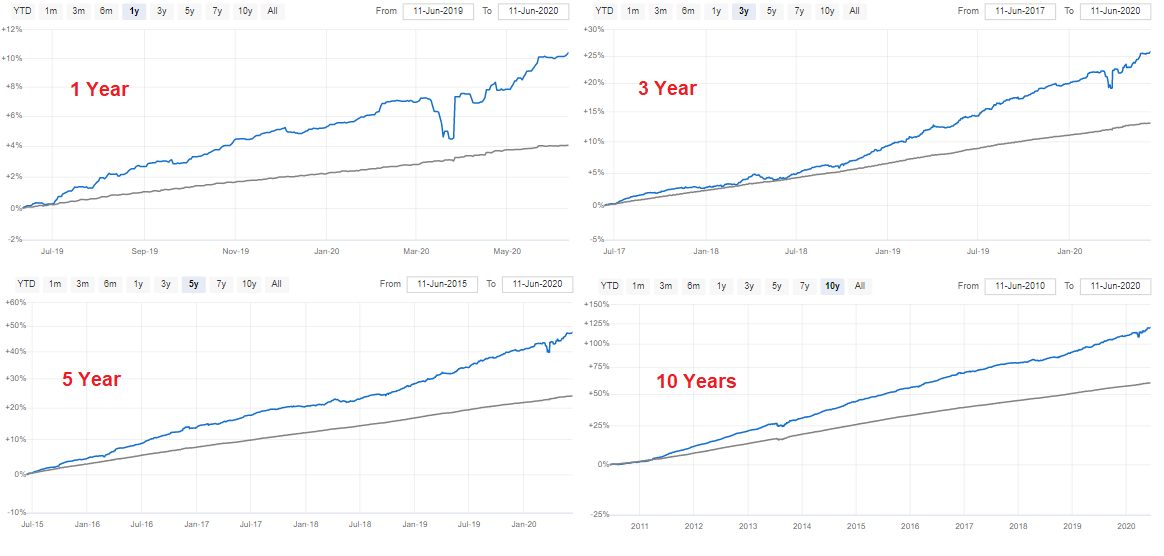

CLICK TO ENLARGE

The longer you wish to stay invested, more predictable will be the return you can generate. A fund which plans to hold its portfolio till maturity, will give you a more predictable projection of returns. Further, the quality of paper which the fund holds will add to that certainty.

Effectively then, a fund which holds Government securities and which plans to hold those securities until maturity, will most likely deliver on its promised return. That being said, if you buy and sell any fund within its maturity profile, your returns could be higher or lower depending upon overall interest rate scenario.

EXAMPLE

In the article that I have quoted above, I had mentioned the Nippon India Nivesh Lakshya Fund on which I have received multiple queries. I will address 2 important queries here to bring out what FD replacement should look like:

- How can a fund deliver higher than FD returns by holding its portfolio till maturity?

- What could go wrong with such a fund?

On Delivering Higher than FD Returns

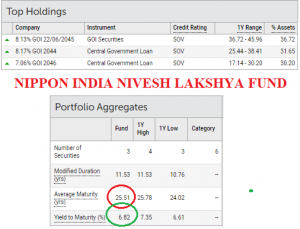

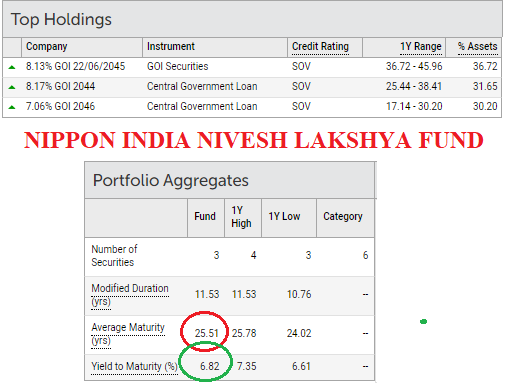

Once you know the Average Maturity of a fund + the fact that the portfolio manager has decided to hold the portfolio till its maturity, you know exactly the Rate of Interest (ROI) you will make on the portfolio. Consider this:

Average Maturity for the above portfolio is 25.51 years. In other words, if you hold this portfolio for this duration, you will make 6.82% return.

Looking at what this portfolio is holding, it becomes clear that this portfolio is safer than any of your Fixed Deposits and makes a higher return, which is tax efficient (i.e. is taxed at 20% after indexation). So why should everyone not be buying this over an FD? After all, the returns are higher and far safer, right?

HERE IS WHY:

YTM at any point is conditioned on the fact that the fund manager will hold this portfolio till maturity.

What happens if the Fund Manager changes the portfolio before Maturity?

In such a scenario, the average maturity and YTM will both change. When choosing to invest long term capital for wealth preservation, you must look for funds which will hold the portfolio till maturity. If you buy for a short term, you may burn your portfolio if RBI raises interest rates.

To sum up (in case of hold to maturity portfolios)

- Price of a bond may increase or decrease with change in interest rates; ultimately however, the bonds will be redeemed at face value.

- Until redemption, the bonds will pay a predetermined rate of interest.

- Hence, if you hold till maturity, you will make a predetermined rate. For example, in the above fund, you will make 6.82% p.a. which will be nearly tax free.

Disclaimer: About the Above Fund

- I have used the Nippon India Nivesh Lakshya Fund for HNI/ UHNI client investments where our clear goal was long term wealth preservation.

- The fund has the flexibility to buy / sell in the existing portfolio.

- The fund manager is clear about holding the portfolio till maturity.

- You should avoid buying this fund if your time horizon is less than 7-8 years, unless you can take some interest rate risk.

- There is a 3 year exit load on the fund.