Federal Bank – Results Expected on 9th May, 2018

Price: Rs. 99 (holding)

Founded in 1931, The Federal Bank Limited (“Federal Bank” or “Bank” or “Company”) is engaged in commercial banking activities in India. The Bank classifies its business in four segments:

1) Treasury; Corporate

2) Wholesale Banking

3) Retail Banking; and

4) Other Banking Operations

Apart from accepting deposits and providing loans, Federal Bank also provides life, health, and general insurance products; mutual funds, online trading facility and earns non-fee based inome from various other service offerings including national pension system, bank guarantee, bill discounting, merchant banking, cash management, depository, E-Commerce, trade finance, ATM, Internet and mobile banking, telephone banking, payment, fund transfer, electronic clearing, safe deposit locker, cash deposit machine, and online tax payment services.

As of March 31, 2017, Federal Bank operated through a network of 1,252 branches and 1,667 ATMs. The Company was formerly known as Travancore Federal Bank Limited and changed its name to The Federal Bank Limited in March 1947. The Company is headquartered in Aluva, India.

Total Deposits for Federal Bank have increased at a CAGR of 70% since FY 2013 with major spur in deposits during the period between FY 2016 and FY 2017.

Operating profit margin and Net Profit margin have reduced over time but is still better as compared to industry standards. In FY 2016-2017, operating profits grew by 16.58% and Net Profit by 74.90%.

| Income | Operating profit | Operating Margins | Net Profit | Net Profit Margins | |

| FY 2013 | 6,911 | 5,501 | 80% | 850 | 12% |

| FY 2014 | 7,691 | 6,027 | 78% | 829 | 11% |

| FY 2015 | 8,366 | 6,665 | 80% | 1,012 | 12% |

| FY 2016 | 8,635 | 6,106 | 71% | 488 | 6% |

| FY 2017 | 9,867 | 7,118 | 72% | 853 | 9% |

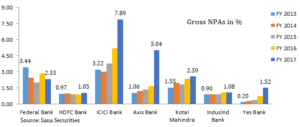

IMPROVING ASSET QUALITY

Non-Performing Assets (NPA) are currently weighing down most public as well as private sector banks. When compared with best of industry players, Federal Bank’s NPA levels have been pretty much under control.

In fact, only Federal Bank’s Gross NPA % has fallen as compared to FY 2013 (in FY 2017). For the rest, it has either risen or has remained same. ICICI, Axis, Yes Bank and Kotak Mahindra banks have all reported consistently higher NPAs.

IMPROVING NET INTEREST MARGINS (NIMS)

CASA ratio and NIMs are two very decisive factors for a bank. A higher CASA ratio is preferred as it reduces the liability of the banks to pay interest on the deposits. Similarly, a higher NIM is preferred as it reflects that interest income earned is higher than the interest paid out. On both the grounds, Federal bank proves to be very competitive in comparison to higher valued peers.

Low cost CASA Deposits for the company have increased by c.23% for the FY 2016 and 2017. Currently the CASA ration for the bank is 32.93%.

Federal Bank’s Net NPA% is also better than its Large cap peers in the likes of ICICI Bank, Axis Bank and Kotak Mahindra Bank.

Some of the features of Federal Bank based Q3 FY 2018 Results

- Total Advances have increased by 22.01% from Rs. 69,629.22 Cr to Rs.84,953.08 Cr.

- Cost to Income Ratio has declined by 159bps from 52.4% to 50.8%

- Gross NPA as a percentage reduced to 2.52% and Net NPA stood at 1.36%

- In terms of Risk Analysis of the asset quality of loans, c.72% of the wholesale loan portfolio which constitutes c.40% of the total loan book is rated A & Above and c.17% is rated in BBB category

- Federal Bank’s Mobile based transactions have increased from Rs. 789 Cr. to Rs. 1535 Cr. showing a tremendous growth of c.95% y-o-y. Also customer base has increased from 5.96 lacs to 9.74 lacs during the same period

- Low cost CASA Deposits for the company have increased by c.4% for the FY 2016 and 2017. Currently the CASA ratio for the bank is 32.96%.

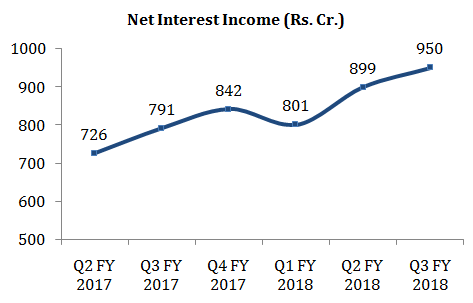

- In the latest quarter (Q3 FY18), the company achieved its highest NII in a quarter of Rs. 950 Cr.

As per the current trends and recent performance, Federal Bank stock is a good buy. With stronger profit growth, lower NPA% and expansionary developments in the online segment, the Bank is at a robust position. It is very competitive when compared with its large cap peers as well. Income growth is strong and continuous.

Thank you!!

Why are you not analyzing with latest results?

will do with a fresh article soon.