Hindalco Industries Limited (“Hindalco” or the “Company”) is an industry leader in aluminium and copper. Hindalco’s acquisition of Aleris Corporation in April 2020, through its subsidiary Novelis Inc., has cemented the company’s position as the world’s largest flat-rolled products player and recycler of aluminium.

Hindalco’s state-of-art copper facility comprises a world-class copper smelter and a fertiliser plant along with a captive jetty. The copper smelter is among Asia’s largest custom smelters at a single location.

Today, Hindalco ranks among the global aluminium majors as an integrated producer.

The Birla Copper unit produces copper cathodes and continuous cast copper rods, along with other by-products, including gold, silver, and DAP fertilisers. It is India’s largest private producer of gold.

Aluminium – One of the largest integrated primary producers of aluminium in Asia. With a pan-Indian presence that encompasses the entire gamut of operations, from bauxite mining, alumina refining, aluminium smelting to downstream rolling, extrusions and recycling, Hindalco enjoys a leadership position in aluminium and downstream value-added products in India.

Copper – Hindalco’s copper facility in India comprises a world-class copper smelter, downstream facilities, a fertiliser plant and a captive jetty. The copper smelter is among the world’s largest custom smelters at a single location.

Hindalco’s global footprint spans 47 manufacturing units across 10 countries.

Financial Performance

| Particulars | FY17 | FY18 | FY19 | FY20 | FY21 |

| Revenue (In Rs. Cr.) | 1,00,183.78 | 1,15,182.80 | 1,30,542.25 | 1,18,144.00 | 1,31,985.00 |

| Growth | – | 14.97% | 13.33% | -9.50% | 11.72% |

| EBITDA (In Rs. Cr.) | 12,447.89 | 13,820.37 | 15,510.52 | 14,306.00 | 17,536.00 |

| EBITDA Margin | 12.43% | 12.00% | 11.88% | 12.11% | 13.29% |

| EBIT (In Rs. Cr.) | 7,979.11 | 9,314.13 | 10,733.54 | 9,215.00 | 10,908.00 |

| EBIT Margin | 7.96% | 8.09% | 8.22% | 7.80% | 8.26% |

| PBT (In Rs. Cr.) | 3,340.03 | 8,282.13 | 8,082.61 | 5,924.00 | 7,905.00 |

| PAT (In Rs. Cr.) | 1,899.74 | 6,082.92 | 5,495.67 | 3,767.00 | 5,182.00 |

| PAT Margin | 1.90% | 5.28% | 4.21% | 3.19% | 3.93% |

| EPS (In Rs.) | 9.07 | 29.03 | 26.22 | 16.93 | 23.29 |

| EPS Growth Rate | – | 220.20% | -9.65% | -35.44% | 37.57% |

| Historic P/E (Closing Price of 31st March) | 20.48 | 7.12 | 7.32 | 6.33 | 14.17 |

| CURRENT P/E | 17.09 | ||||

| D/E | 1.27 | 0.93 | 0.91 | 1.15 | 0.98 |

| EV/Sales | 0.68 | 0.78 | 0.62 | 0.61 | 1.06 |

| EV/EBITDA | 5.50 | 6.48 | 5.25 | 5.03 | 7.96 |

| Interest Coverage | 2.17 | 3.53 | 4.11 | 3.41 | 4.69 |

| ROCE | 7.63% | 8.78% | 9.78% | 7.35% | 8.29% |

| ROE | 4.12% | 11.09% | 9.56% | 6.46% | 7.79% |

Quarterly Performance

| Q4 FY 2020 | Q1 FY 2021 | Q2 FY 2021 | Q3 FY 2021 | Q4 FY 2021 | TTM | Q-o-Q % | Y-o-Y

% |

|

| Revenue | 29,318.0 | 25,283.0 | 31,237.0 | 34,958 | 40,507 | 1,31,985 | 15.87% | 38.16% |

| EBITDA | 3,840.00 | 1,933.00 | 4,750.00 | 5,198.0 | 5,655.0 | 17,536.0 | 8.79% | 47.27% |

| EBITDA Margin | 13.10% | 7.65% | 15.21% | 14.87% | 13.96% | 13.29% | ||

| PAT | 668.00 | -569.00 | 1,785.00 | 2,021.0 | 1,945.0 | 5,182.00 | -3.76% | 191.17% |

| PAT Margin | 2.28% | -2.25% | 5.71% | 5.78% | 4.80% | 3.93% | ||

| EPS | 3.01 | -2.56 | 8.03 | 9.08 | 8.74 | 23.29 | -3.74% | 190.37% |

Q4 Highlights:

- Novelis Net Income from continuing operations at $180 million ($63 million), up 186% YoY

- Record quarterly Aluminium India Business VAP (excluding wire rods) sales at 92Kt up 21% YoY reaching 28% of total metal sales

- Board recommends dividend @300% (₹3/share) for FY21 as against 100%(₹1/share) for FY20.

Business Segment Performance in Q4 FY21 (vs Q4 FY20)

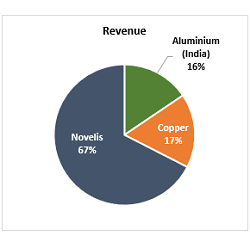

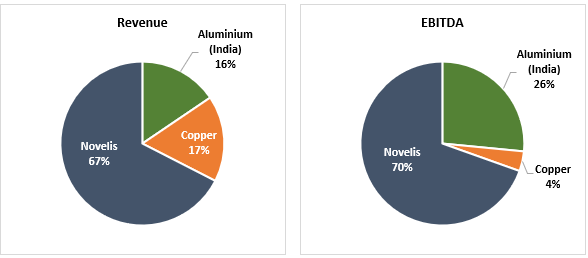

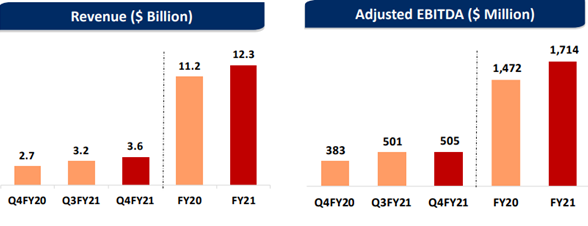

[1] Novelis (including Aleris) – Novelis recorded its best-ever quarterly adjusted EBITDA of $505 million (vs $383 million), up 32% YoY, on the back of higher organic volume, favourable metal benefits, and a US$60 million EBITDA contribution from the acquired Aleris business.

[2] Aluminium India – EBITDA was at an all-time high of ₹1,610 crore in Q4 FY21, compared with ₹1,043 crore for Q4 FY20, an increase of 54% YoY, primarily due to favourable macros, better operational efficiencies and lower input costs. EBITDA margin of 27% was the highest in the last 12 quarters and continues to be amongst the best in the industry. Revenue was ₹5,969 crore in Q4 FY21 vs ₹5,299 crore in the prior year period.

[3] Copper – Copper Cathode production was at 97 Kt in Q4 FY21 (vs 75 Kt in Q4 FY20), higher by 29% YoY on account of stable operations during the quarter. Revenue from the Copper Business was ₹8,508 crore this quarter, up 80% YoY, primarily due to higher global prices of copper.

INVESTMENT RATIONALE

-

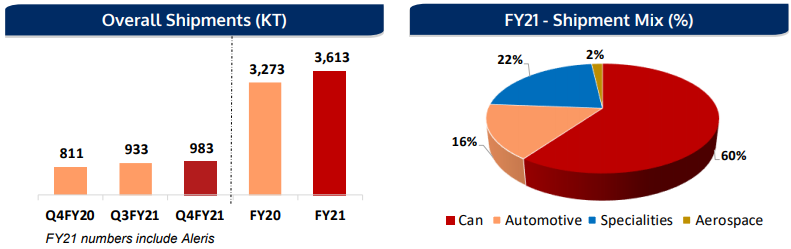

- Aleris Acquisition in 2020 – The completion of the Aleris acquisition by its wholly-owned subsidiary Novelis Inc. has positioned Hindalco as one of the world’s largest aluminium companies, with a global footprint spanning 49 state-of-the-art manufacturing facilities in North America, Europe and Asia. The Aleris business continues to positively impact the overall top line and EBITDA. During Q4 FY 2021, Novelis recorded its best-ever quarterly adjusted EBITDA of $505 million (vs $383 million), up 32% YoY, on the back of higher organic volume, favourable metal benefits, and a US$60 million EBITDA contribution from the acquired Aleris business. Total shipments of flat rolled products (FRPs) were at an all-time high of 983 Kt (vs 811Kt), up 21% YoY, with the addition of the acquired Aleris business and strong demand across end-product markets.

- Expansion Project Updates – Automotive finishing plants at Guthrie, Kentucky, in the U.S. and Changzhou in China, were both commissioned during FY21 and started its commercial shipments in Q4FY21. This will increase Novelis global automotive finishing capacity to ~1 mn tons. The Company also updated that Recycling, Casting and Rolling expansion in Pinda, Brazil remains on track with Recycling to commission in Q1 FY22 and rolling capacity to commission in end of FY22.

- Utkal Expansion: Commissioning of Utkal 500ktpa refinery expansion would take place in 1QFY22. Cost of production at the Utkal refinery is ~50% of other alumina refineries, which would lead to cost savings. The Company would rampdown Renukoot refinery as Utkal refinery ramps up. It plans to sell half of Utkal production in the market once Utkal refinery ramps up fully.

- FY 2021 witnessed faster-than-expected recovery from the second quarter onwards after the first quarter saw demand impacted by the pandemic. Healthy demand from beverage can segment, coupled with recovery in demand from auto and specialties resulted in improved profitability for Novelis. Adjusted EBITDA per tonne increased to more than USD 500 in the third quarter of fiscal 2021 from less than USD 330 per tonne during the first quarter. Recovery in aluminium demand, along with higher London Metal Exchange (LME) prices, also led to strong improvement in domestic profitability.

- Healthy Operating Efficiency of Domestic Aluminium Operations – Hindalco benefits from a fairly low cost of production for the aluminium operations, with its smelters occupying a first or second quartile position in global cost curves. The Company also benefits from full alumina integration with captive bauxite mines, and relative stability in coal costs with about 90% coal security through a combination of linkage from Coal India Ltd and captive coal blocks. During Q4 FY 2021, the Company posted record quarterly EBITDA of Rs. 1,610 Cr. (Rs.1,043 Cr.) up 54%, on account of favourable macros, better operational efficiencies and lower input costs