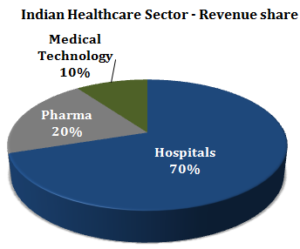

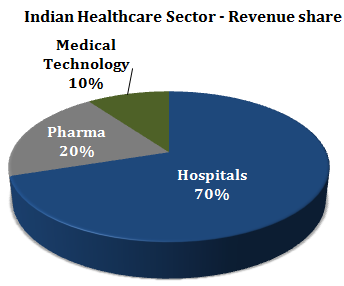

Hospitals constitute ~70% of Indian healthcare market with increasingly dominant role of private sector. Private players have established a dominating presence in specialty health care. The market size of private hospitals is expected to grow at a CAGR of 19.2 % to reach ~U.S. $ 120 billion by 2020 from its current size of ~U.S. $ 50 billion.

Key Drivers for Growth of Hospital Business in India

- 500 Million Additional middle class by 2025.

- Less than 25% of population is currently covered by insurance. At the current rate of growth of insurance business the Insurance penetration is likely to reach up to ~ 45% of population by 2020.

- Growth in insurance business is most positive for private sector hospitals. Health insurance provides affordability to high end medical treatment.

- Medical Tourism will be an added boost given the cost of high quality medical treatment which Max India provides.

COMPARATIVE ANALYSIS FOR HOSPITAL STOCKS – MAX INDIA, APOLLO HOSPITALS AND FORTIS HEALTHCARE

** The figures below are based on share of business for hospital segments (excludes insurance, pathology and pharmacy businesses)

| Metric | MAX | APOLLO | FORTIS |

| Operational Beds | 2,200 | 6,724 | 3,600 |

| No. of Hospitals | 13 | 69 | 54 |

| Presence | North India | Pan India | Pan India |

| Revenue (Rs. Cr.) | 2,098 | 5,409 | 3,449 |

| Growth (%) | 24% | 18% | 8% |

| EBITDA (Rs. Cr.) | 215 | 741 | 508 |

| Growth (%) | 26% | 9.2% | 11 % |

| EBITDA Margin | 10.2% | 13.7% | 14.7% |

| ROCE (%) | 4.6% | 11% | 1.3% |

| ARPOB (Rs./day) | 40,902 | 28,036 | 37,534 |

MAX INDIA

Max India (“Max India” or the “Company”) has split its business across (i) Hospitals; (ii) Health Insurance and (iii) Senior Living Facility (yet to start operations).

BUSINESS DIVISIONS

Hospitals: The Company has a strong presence in in North India, with over 10 hospitals in Delhi & NCR and others in Mohali, Bathinda and Dehradun with 2,200 beds.

Health Insurance: Max Bupa Health Insurance Limited – a 51:49 joint venture between Max India and Bupa Finance. Max Bupa operates through a network of 26 offices across 13 cities and has a customer base of 1.4 million.

Expansion plan – Max India is expected to double its bed strength this year (FY 2017) from current 2,200 to 5,000 after its 2 acquisitions, namely – Saket City Hospital, and Pushpanjali Hospital in Shalimar Bagh, Delhi. Also, Max Bupa network grew by 28% in FY 2016 and the management expects health insurance operations to become profitable over the next 3-4 years.

APOLLO HOSPITALS

Apollo Hospitals Enterprise (“Apollo Hospitals” or the “Company“) is a private healthcare provider in Asia with hospitals in India, Sri Lanka, Bangladesh, Ghana, Nigeria, Republic of Mauritius, Qatar, Oman and Kuwait.

The Company’s key businesses include:

Healthcare Services: The Company operates as the largest hospital networks in Asia with 6,724 owned and 1,434 managed beds across 61 owned and 8 managed hospitals (as on March 31, 2016).

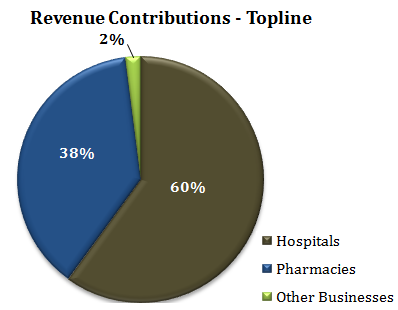

Standalone Pharmacies: Apollo Hospitals operates a large network of pharmacies in India with 2,326 outlets across 22 states (as on March 31, 2016).

Other Businesses: The Company’s other businesses include Clinics, Health Insurance (in a joint venture with European Insurer Munich Health Holding AG), healthcare project and consultancy services, healthcare BPO, health education, and research.

Expansion plan – The Company is planning to expand its bed capacity by adding 1,045 beds with total estimated project cost of 1,520 Cr. by FY 2019.

| Location | No. Of Beds | Estimated Project Cost (Rs. Cr.) |

| Addition in FY 2017 | ||

| Indore (expansion) | 65 | 28 |

| Navi Mumbai | 480 | 602.4 |

| Total | 545 | 630.4 |

| Addition in FY 2019 | ||

| South Chennai | 200 | 750 |

| Byculla, Mumbai | 300 | 140 |

| Total | 500 | 890 |

FORTIS HEALTHCARE

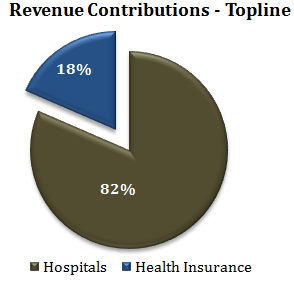

Fortis Healthcare Limited (“Fortis Healthcare” or the “Company”) operates with 45 healthcare facilities with presence across 14 states and 19 cities, 3,600 operational beds, 329 diagnostic centers and over 7,300 collection points. The Company generates 82% of its revenue from hospital business and the rest from diagnostic business.

IMPORTANT UPDATE – DEMERGER OF DIAGNOSTICS BUSINESS (SRL LIMITED)

| Step 1 (a) | Rationale | Consideration |

| Transfer of the Hospital Business of Fortis Malar to Fortis Healthcare by way of slump sale. Fortis Malar to retain its existing diagnostic business | To keep the hospital business under one entity i.e. Fortis Healthcare. | Fortis Healthcare to pay a cash consideration to Fortis Malar of Rs. 43 Cr. |

| Step 1 (b) | Rationale | Consideration |

| Demerger of business undertaking comprising the diagnostic business in Fortis Healthcare to Fortis Malar | To keep the diagnostic business under one entity i.e. Fortis Malar | Fortis Malar to allot its shares to shareholders of Fortis Healthcare.

Share entitlement ratio of 0.98 : 1 |

| Step 2 | Rationale | Consideration |

| Merger of SRL into Fortis Malar. Name of Fortis Malar shall be changed to SRL Ltd | To house the entire diagnostic business directly under Fortis Malar | Fortis Malar to allot its shares to shareholders of SRL (excluding itself).

Share exchange ratio of 10.8 : 1 |

The date for the slump sale, demerger and merger under the composite scheme is January 1, 2017.

Hi Rajat, that is a good write-up. Is there any particular reason for not considering Indraprastha Medical? It probably has got good fundamentals too, a small cap stock.

On a different subject, few months ago you have written about Schneider Electric, in the similar space TD Power Systems operate too. I would like to see your take on it.

Keep up the good work!

Regards,

Ram

So which company to choose if I want to invest in SRL diagnostic?

I like Max India