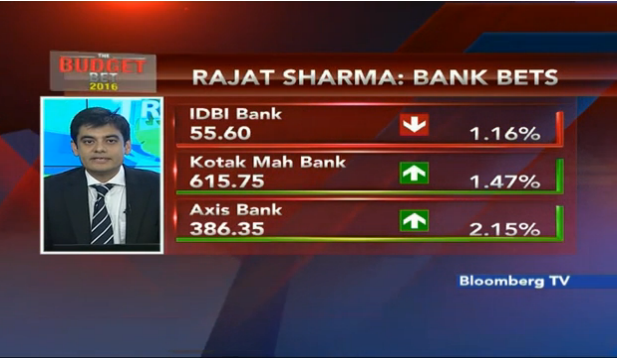

Just before the union budget, I recommended 2 PSU banks that you could buy – IDBI Bank and State Bank of India (SBI).

Click the video below:

DATE: 29 February 2016

Watch 6:20 Onward.

Watch 6:20 Onward.

Of course I have been negative on PSU Banks for 4 years. Let me take you back a few years to my initial reasons:

1. Poor Service – I doubt if PSU Banks can eat into the market share of private banks with the kind of difference you see in service standards.

2. No Accountability of management – There is a reason why PSU banks are facing this NPA mess. Think about it – why is the problem so big for PSU banks and how private sector banks managed to avoid risky/ sub-standard loans? In fact, think about this – with NPA levels over 10% in at least 5 PSU banks, how is it that none from amongst the current and previous management is being questioned about the kind of loans that were extended in past?

3. Political interference – Here I am not only talking about extending loans without proper diligence to those who close to the establishment. The problem is far bigger. I think government banks must get into ‘farm loan waivers’ and other social schemes from time to time, whether they want to or not. I’d rather look at banking as a business for creating shareholder return over social welfare that’s all.

I think over the last 2 years, there has been some improvement (at least optically), in accountability and political interference. Service however has remained as poor as ever. The other thing that hasn’t changed at all is stock prices, if at all they have depreciated in most cases.

Am I Now Bullish on PSU Banks?

Short answer – No, for most part.

For a moment forget about how much PSU bank stocks have corrected. Now make a list of reasons why you want to buy anything here, without focusing on the price. I think in large part people want to buy in this space only because some of these stocks have fallen so much and so they appear really cheap.

Reasons for Recommending IDBI Bank and State bank of India

The worry for the PSU banking space is this – how deep the crisis could be?

The way PSU banks have come out and declared their NPAs and taken a hit on profitability, I get a sense that there is concerted effort on the part of RBI and the government to clean things up. But have these banks declared everything or is there more pain left. Frankly nobody knows but it’s true that these NPAs were declared following an asset quality review (AQR) initiated by the Reserve Bank of India (RBI).

When the tide turns and corporate India need quick loans without the stringent diligence carried out by private sector banks, it will again be the state run banks which will handhold businesses and help them expand. Remember how SBI helped Tata Motors in its bid for JLR.

DATE: 23 February 2016

Watch for banking stocks from 4.50 onwards

For these reasons I would have liked to allocate some money to the PSU banking space, particularly to IDBI Bank and State Bank of India.

Why IDBI Bank?

This is based on balancing how bad things could be (which is a pure guess) vs. how much the stock has corrected. Additionally:

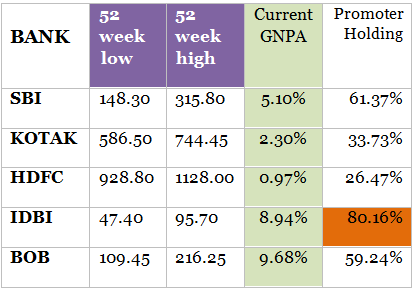

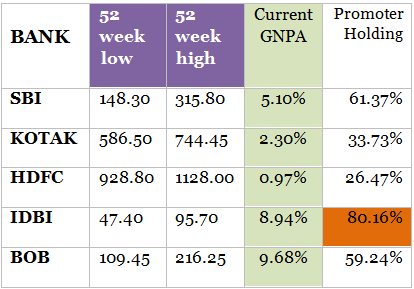

- IDBI Bank has 80% government holding which gives the government ample headroom to divest

- IDBI Bank is in the process of raising Rs.3, 771 Cr. through qualified institutional placement (QIP) route.

- IDBI Bank is planning to sell 600 Cr of non core asset. Quite apart, among all PSU banks, IDBI has one of the largest land bank and properties in top cities of the country purchased almost a century back. They could actually deal with this NPA mess by selling some of their properties in Mumbai and Delhi alone. The bigger problem is – lack of urgency in dealing with this problem.

- Encouraging commentary: Despite the fact that NPAs have gone up from 5-6%, to now 9% in Q3 of 2016, the management has said they do not need any more capital from the government and will be adequately capitalized.

Government plans to transfer IDBI bank’s Bad Loans to special Entity (announced last year) and has in the budget announced that it will bring its shareholding below 50% in IDBI Bank, to privatize it on the lines of Axis Bank.

Why State Bank of India?

Just as I said in the video above, you can not have the market cap of SBI equaling that of Kotak Mahindra Bank. Nothing can convince me that these banks should enjoy similar kind of brand equity. Here’s a stat – Kotak Mahindra number of branches: 1298 | SBI number of branches: 16,333 (as of early last year).

A lot can be written on this topic and it will all will be divided between those who will swear by pvt banks and those who may now prefer to invest in PSUs. Even without getting into much detailed financial analysis, I am convinced that it is time to allocate some money to this space, even though I do not hope for any out-performance in a hurry.