IPCA Laboratories Limited (“IPCA” or the “Company”) is one of the world’s largest manufacturers and suppliers of over a dozen APIs. The Company’s product range includes pain management, cardiovascular medicines, anti-malarial, anti-emetic, antibiotic, analgesic, and anti-diabetic; and formulations for cough and cold therapy, skin problems, and problems with the central nervous system.

IPCA Laboratories Limited (“IPCA” or the “Company”) is one of the world’s largest manufacturers and suppliers of over a dozen APIs. The Company’s product range includes pain management, cardiovascular medicines, anti-malarial, anti-emetic, antibiotic, analgesic, and anti-diabetic; and formulations for cough and cold therapy, skin problems, and problems with the central nervous system.

The Company is also a leading supplier of APIs such as atenolol (anti-hypertensive), chloroquine and artemisinin derivatives (anti-malarial), furosemide (diuretic), and pyrantel salts (anthelmintic).

Financial Performance

| Particulars (Rs. Cr.) | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2019-20 |

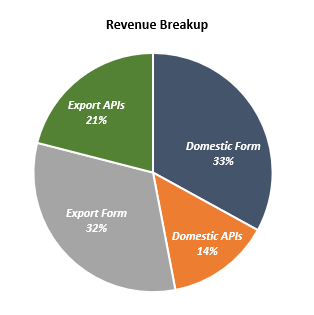

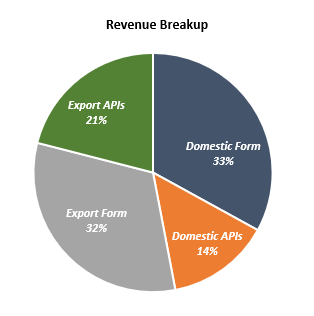

| Domestic Income | 1,440.88 | 1,617.13 | 1,694.54 | 1,956.90 | 2,288.37 |

| Exports Income | 1,429.85 | 1,561.74 | 1,564.21 | 1,730.84 | 2,143.75 |

| Total Income | 2,870.73 | 3,178.87 | 3,258.75 | 3,687.74 | 4,432.12 |

| EBITDA | 341.81 | 435.20 | 478.82 | 765.26 | 993.41 |

| EBITDA Margin % | 0.12 | 0.14 | 0.15 | 0.21 | 0.22 |

| Profit Before Tax | 111.45 | 258.20 | 282.80 | 557.39 | 784.97 |

| Net Profit After Tax | 92.52 | 188.29 | 233.11 | 454.91 | 652.46 |

| Net Profit Margin (%) | 0.03 | 0.06 | 0.07 | 0.12 | 0.15 |

| Earnings Per Share (Rs.) | 7.33 | 14.92 | 18.47 | 36.01 | 51.64 |

| Share Capital | 25.24 | 25.24 | 25.24 | 25.27 | 25.27 |

| Reserves and Surplus | 2,257.81 | 2,449.88 | 2,669.71 | 3,111.41 | 3,652.27 |

| Net Worth | 2,283.05 | 2,475.12 | 2,694.95 | 3,136.68 | 3,677.54 |

| Dividend (%) | – | 50% | 50% | 150% | 250% |

WHAT’S DRIVING/DRAGGING THE STOCK?

Leader in The Anti-Malarial Space

IPCA is a fully integrated Indian pharmaceutical company, manufacturing more than 350 formulations and 80 APIs for various therapeutic segments. IPCA is a leader in the anti-malarial space with a market share of over 34% with a fast-growing presence in the international market as well.

Strong Quarterly Performance

IPCA is a leader in the anti-malarial space and has presence in other therapy areas as well. The Company reported strong performance for the quarter backed by an impressive growth in the API segment. The Company reported revenues at Rs 1534 Cr., up 42.3% y-o-y backed by 72% y-o-y growth in the API segment. The quarter also reflected incremental sales from Covid related medicines – Hydrooxychloroquine (HCQS) and Chloroquine (CHQ). Together both these medicines accounted for around Rs 260 Cr. of revenues.

India formulations accounted for 50% of sales in Q1 FY21. The lockdown had a 12% impact on its India business growth. Key therapies impacted INCLUDES anti-bacterials, dermatologicals and ophthalmologicals.

New Capacity Expansion

The Company is in the process of setting up a new APIs manufacturing unit at Dewas (M.P.) with an initial capital outlay of about Rs. 300 Cr., of which the Company plans to spend around Rs.50-60 Cr. in FY2021. Ipca has received environmental clearance of the facility and plans to commence construction October 2020. The management expects the plant to be ready within the next 15 months.

FY 2021 Guidance

The Company expects that Chloroquine/HCQS based opportunities are expected to wane, going ahead. Also, the Company is witnessing a decline in malaria cases amid Covid-19 lockdown and precautions. The management has guided for 15-19% sales growth in FY21 if the domestic formulations market recovers and expects APIs to grow 20% in FY21.

Facilities Under U.S. FDA Scrutiny

IPCA’s Pithampur and Pipariya facilities have been under the USFDA scrutiny. The company has completed the remediation process as well as the submission to the regulator. A reply from the regulator is awaited. Though in the light of Covid pandemic, IPCA expects a possible delay in the re-inspection of the plants.