Price – Rs. 1,285 (After adjusting for June 2017 Bonus- 1764)**

16 December, 2015

VIEW – BUY

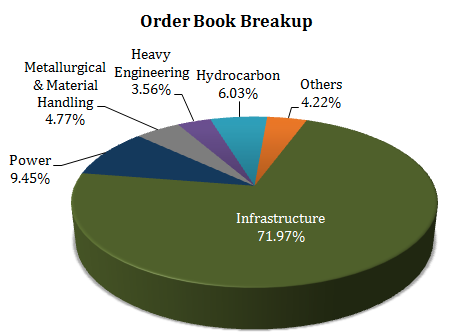

Larsen & Toubro Limited (“L&T” or the “Company”) has business interests in sectors ranging from engineering, construction, manufacturing, information technology and financial services. It has a dominant presence in India’s infrastructure, power, hydrocarbon, machinery and railway-related projects.

► Infrastructure segment comprises engineering and construction of building and factories, transportation infrastructure, heavy civil infrastructure, power transmission & distribution and water & renewable energy projects.

► Power segment comprises turnkey solutions for coal-based and gas-based thermal power plants including power generation equipment.

► Metallurgical & Material Handling segment comprises turnkey solutions for ferrous (iron & steel) and non-ferrous (aluminium, copper, lead & zinc) metal industries, bulk material & ash handling systems in power, port, steel and mining sector including manufacture and sale of industrial machinery and equipment.

► Heavy Engineering segment comprises manufacture and supply of custom designed, engineered equipment & systems to core sector industries like refinery, petrochemical, chemical, oil & gas, aerospace and defence.

► Electrical & Automation segment comprises manufacture and sale of low and medium voltage switchgear components, custom built low and medium voltage switchboards, electronic energy meters systems and control & automation products.

► Other segment includes realty, shipbuilding, marketing and servicing of construction & mining machinery, manufacture and sale of rubber processing machinery

INVESTMENT RATIONALE

Strong Order Book

Larsen & Toubro has bagged many orders in promising segments such as urban infrastructure, water, civil engineering, hydrocarbons and power in the past year.

Over the past five years, order inflow has grown at a CAGR of 8 %. The Company has already bagged more than Rs. 54,996 Cr. new orders so far this fiscal i.e. FY 2016. The Company’s consolidated order book stands at Rs. 2, 44,097 Cr. as at September 30, 2015, higher by 14% on a y-o-y basis with international order book constituting 28% of the order book. The increase in the order book lends long term earnings visibility.

The Company expects ordering activity to pick up in India. There are strong prospects in roads, power T&D, oil and gas (both upstream and downstream), urban infra and fertilizers. Defence and nuclear projects are exciting prospects but can translate into revenues in FY 2018.

Proxy play on India infrastructure story

Government Initiative – The Indian Infrastructure sector is likely to get major boost from the Government’s focus on development of infrastructure in India. In the Union Budget for 2015-16, total investment in infrastructure is proposed to be increased by Rs. 700 billion over 2014-15.

L&T continues to be the best play in the Indian infrastructure space, given its strong business model (diversified with a presence across all segments of infrastructure i.e. power, roads, hydrocarbons & process industries), diverse skill sets, strong execution capabilities and relatively healthy balance sheet.

The Company is also focusing to scale up its operations in niche areas like defence, nuclear power & shipbuilding that have the potential to add significantly to overall revenues in the next three to five years (for example, opening of defence FDI can help L&T to increase its scale of operations 5 times in terms of defence segment revenues, according to management).

Given the Company’s market positioning, Larsen & Toubro is well positioned to gain from an expected gradual recovery in the capital expenditure cycle, given its exposure to a range of sectors, and better cash flow generating potential vis-a-vis its peers.

Strong Financial Position

Larsen & Toubro has shown consistent growth over the last 10 years (i.e. 2005-06 to 2014-15). Its net revenue from operations over this period grew at an impressive CAGR of 40.88%. For FY 2015, income from operations increased by 8.08 % to Rs. 92,004.58 Cr. from Rs. 85,128.40 Cr. and EBITDA increased by 5.40 % to Rs. 11,335.61 Cr. from Rs. 10,754.34 Cr. The Company has reserves in excess of Rs. 40,723.16 Cr.

At CMP of Rs. 1,296.35 (16th December, 2015), Larsen & Toubro is trading at a P/E of 25.30x. The Company has paid consistent dividend. The Company has consistently paid a dividend in the range of Rs. 12 – Rs.15 over the past 4-5 years and has maintained an average dividend yield of 1.20% over the last 5 financial years.

L&T’s average long term debt to equity ratio over the last 5 financial years has been 1.24 times.

INVESTMENT CONCERNS

While infrastructure theme is likely to do well for many years given the need for infrastructure projects in India, this is one sector where investors have to be extremely careful in making stock selection.

Also see: Best Infrastructure Stocks in India

Intense Competition

Competition for L&T has increased over the past few years. The Company operates in a highly competitive business, especially when it comes to low to medium engineering and construction projects. Even for the complex and high-value projects where L&T has a stronghold, competition from both Indian and foreign companies are on a fast rise.

Further, competitors are also trying to catch up the Company’s quality and size, which will put pressure on L&T profit margins in the coming years.

Slowdown in Economy, Decelerating Investment Plans

Despite the immense growth potential, L&T’s growth and profitability is highly dependent on the growth of Indian economy and the infrastructure spending of the Indian government. Any slowdown in the broad economy will impact L&T’s operations.

Further, L&T business is cyclical in nature. For example: there will be slowdown in the new order inflow of the Company when there is a decline in the industrial activities.

Also, any political instability could impact the Company’s plans and, in turn, its revenue stream and profitability.

Risks Relating to Infrastructure Projects

Infra and Engineering Sector is a highly capital-intensive industry with long gestation periods. Revenue generation could take many years after the initial conceptualization of a project. Since most of the projects have a long gestation period (4-5 years of construction period), the uncertainties and risks involved are high.

Delay in commissioning of projects is also a concern as it leads to delay in inflow of revenues. At the same time, companies have to incur costs on the delayed projects, thus affecting margins and overall profitability which could have a negative impact on the share price.

fantastic analysis

Thanks Ravi

Bought 38 Qty @1294 on your advice. Hope for the best..