Date – 31 July, 2018

Price – Rs. 120.60

WHAT’S DRAGGING THE STOCK

Resignation of Deloitte as Auditors

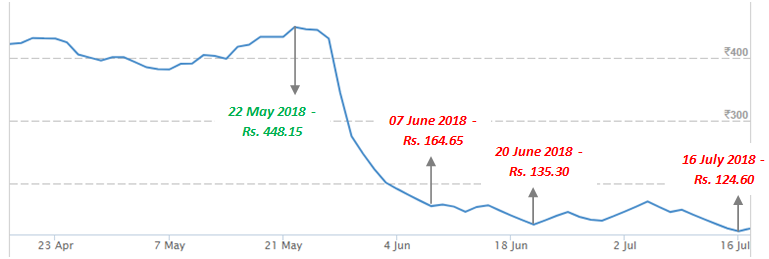

Manpasand Beverages stock tumbled more than 67% from Rs 448.15 on May 22, 2018 to Rs 149.15 on 22nd June 2018.

Reason being: Deloitte Haskins & Sell, the Company’s auditor has quit, a few days before the declaration of annual results. Deloitte’s move was triggered by the lack of cooperation from Manpasand on sharing with the auditor some crucial data related to capital expenditure and revenue.

Retail shareholders are the last ones to know about troubles brewing in companies and hence get deeply impacted by such events that have unfolded in the case of Manpasand Beverages.

Manpasand Beverages Ltd (“MBL” or the “Company”) is engaged in the business of manufacturing of fruit juices in the beverages segment. The Company offers mango-based fruit drink under the Mango Sip brand. The Company also offers its products in other brands, including Fruits Up, Manpasand Oral Rehydrating Salts, Pure Sip and Coco Sip.

- Fruit Up Brand – Fruit drinks and carbonated fruit drinks in various flavors

- Manpasand Oral Rehydrating Salts Brand – Fruit drinks with energy replenishing qualities with a primary focus on North East India. Products – MANPASAND ORS APPLE DRINK and MANPASAND ORS ORANGE DRINK.

The Company’s plants are located at Vadodara, Gujarat; Varanasi, Uttar Pradesh, and Dehradun, Uttrakhand.

MANPASAND BEVERAGES FINANCIAL POSITION

| PARTICULARS | FY15 | FY16 | FY17 | FY18 |

| Revenue from operations | 359.75 | 556.71 | 717.11 | 955.17 |

| Total Expenses | 295.64 | 446.30 | 577.34 | 777.52 |

| EBIDTA | 64.11 | 110.41 | 139.77 | 177.65 |

| Depreciation & amortization expenses | 20.53 | 57.09 | 73.76 | 86.61 |

| EBIT | 43.58 | 53.32 | 66.01 | 91.04 |

| Finance Costs | 10.65 | 5.72 | 1.18 | 2.92 |

| Other Income | 0.41 | 9.13 | 17.91 | 29.78 |

| PROFIT BEFORE TAX | 33.34 | 56.73 | 82.74 | 117.90 |

| Total Tax Expenses | 3.40 | 6.18 | 10.11 | 17.91 |

| PROFIT AFTER TAX | 29.94 | 50.55 | 72.63 | 99.99 |

| Earnings Per Share | 4.71 | 5.40 | 6.35 | 8.74 |

| PARTICULARS | FY15 | FY16 | FY17 | FY18 |

| EBIDTA Margin | 17.82% | 19.83% | 19.49% | 18.60% |

| Net Profit Margin | 8.32% | 9.08% | 10.13% | 10.47% |

Balance Sheet Position

| PARTICULARS | FY15 | FY16 | FY17 | FY18 |

| Share Capital | 37.55 | 50.05 | 57.22 | 114.46 |

| Reserves and Surplus | 153.36 | 551.51 | 1,096.30 | 1,132.07 |

| Net Worth | 190.91 | 601.56 | 1,153.52 | 1,246.53 |

| Long Term Borrowings | 49.16 | – | 0.25 | 0.46 |

| Deferred Tax Liabilities | – | – | – | 0.16 |

| Long Term Provisions | 0.35 | – | – | – |

| Current Liabilities | 110.07 | 59.35 | 79.81 | 178.42 |

| Total Liabilities | 350.49 | 660.91 | 1,233.58 | 1,425.57 |

| PARTICULARS | FY15 | FY16 | FY17 | FY18 |

| Tangible Assets | 216.21 | 402.22 | 454.68 | 715.1 |

| Intangible Assets | 0.09 | 0.09 | 0.23 | 0.14 |

| Long Term Loans And Advances | 25.59 | 19.77 | – | – |

| Other Non-Current Assets | 0.12 | 0.07 | 330.22 | 259.22 |

| Total Current Assets | 108.49 | 238.77 | 448.45 | 451.27 |

| Total Assets | 350.50 | 660.92 | 1,233.58 | 1,425.71 |

Efficiency Ratios

| PARTICULARS | FY15 | FY16 | FY17 | FY18 |

| Return on Equity | 18.15% | 8.86% | 5.72% | 7.30% |

| Return on Capital | 15.68% | 8.40% | 6.30% | 8.02% |

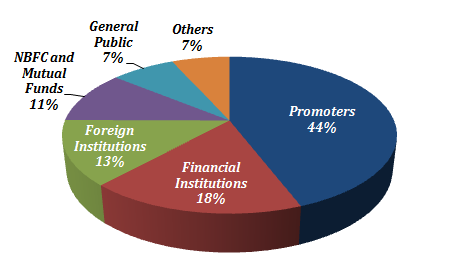

Shareholding Pattern

Company Claims Strong Market Position in the Fruit Drink Segment

MBL’s healthy market position in the fruit drink segment is underpinned by presence of brand Mango Sip (4.5% market share). The Company has made several innovations in the past couple of years, which have enabled it to enter in top 5 players in the mango-based drinks market.

In FY 2014, the Company launched the Fruits up brand in the carbonated drink market. The brand grew 71.30% over the past three fiscals and contributed 25% to the Company’s revenue in FY 2018. With network of 4000 distributors across the country and strong presence in Western and northern parts of India, revenue increased significantly over five fiscal through 2018. These claims have been reeatedly questioned by various analysts.

Mango Sip and Fruits Up remain the main revenue and profit drivers for MBL. Diversification of the product profile through successful new launches is likely to help the Company sustain healthy growth, and will be critical to reduce dependence on a few brands.

Healthy Operating Efficiency

MBL has five plants across Vadodara, Varanasi, and Ambala, in proximity to high-consumption states, which helps the Company to optimize its logistics cost. Furthermore, commissioning of its plant in Sri City (Tamil Nadu) and additional plant in Varanasi and Vadodara in FY 2018 will improve its reach in South India and central India. Manpasand Beverages plans to come up with a plant in East India.

These factors, along with strong procurement setup for fruit concentrate and distribution network (providing reach to 4 lakh outlets across India), efficient supply chain management system, and prudent risk management enable healthy operating efficiency.

Huge Capital Expenditure to Be Partly Funded Through Debt

Manpasand Beverages plans capex of Rs 900.00 Cr. to increase manufacturing capacity with plants at Sri City, Vadodara, Varanasi, and in East India. Capital expenditure will be funded through available liquid fund, healthy cash accrual, and through debt.

However, expected borrowings will not have major impact on financial risk profile considering strong net-worth. Also, stabilization of operations after the capex and achievement of expected operating efficiency will be key sensitivity factors.

Strong Financial Risk Profile

MBL’s financial risk profile is supported by healthy cash position and negligible debt on its book, translating in healthy credit metrics. Net-worth has increased over the years due to equity infusion through initial public offer of Rs 400.00 Cr. in FY 2016 and qualified institutional placement of Rs 500 Cr. in FY 2017.

Strong net-worth of Rs 1,246.53 Cr. as on March 31, 2018, and negligible debt of Rs. 0.46 Cr. shows strong capital structure.

Exposure to Intense Competition

There are many organized and unorganized players across segments in the FMCG space. Also, increasing focus on health and growing popularity of fruit juice products have led to other established FMCG players launching products with similar positioning as current players.

Increase in competition necessitates higher advertising and promotion expenditure. This results in constant need to innovate in terms of packaging, and bringing on refreshes to keep established brands going. Also, new brands require sustained sales promotion until products achieve scale.

Multinational corporations with deep pockets and focus on carbonated products are enhancing investments in the fruit juice segment, impacting margins for other players. Therefore, players such as MBL need to regularly introduce and innovate products, introduce differentiators and refreshes, and build on their reach and distribution to sustain market share as well as profitability

If it is a buying opportunity then what’s the target ?

its an avoid opportunity

Even if audited financials have been signed by new auditor without much variation, what is reason for everyone to be skeptical. The possible reason may be that the audited numbers are not reliable then why no action taken against the Auditors after due scrutiny.

Deloitte resigned after 8 years, if there is any issues with Financials it could have been built up over period of time and why not action to be taken after due scrutiny against Deloitte

Let me know if you find out the answer to any of your questions above 🙂

your view on life insurance business in india with data as i like to invest in insurance stocks