Ratio analysis involves a mathematical interpretation of the financial records of a company, in order to understand its past performance and future prospects. Ratio analysis is an important tool for understanding the financial health of a company and for analyzing the progress of the business.

While conducting ratio analysis it is important to keep some key points in mind:

[I] Study the ratios in totality – never get carried away with the strength of a (single) ratio. It is easy to make one ratio look good at the cost of making another ratio look bad.

Remember, no single ratio can provide a perfect tool for examining a business and in order to conduct a meaningful financial analysis, it is most critical to understand some key ratios in totality and not in isolation.

Example, it is easy to achieve an extremely healthy current ratio by selling off assets and putting money in the bank irrespective of whether the sold assets were profitable or a liability. On the other hand a bad current ratio may well be the result of some long term capital intensive plan.

Before making any analysis on the basis of ratios, to keep in mind that there are several factors which may affect a single ratio.

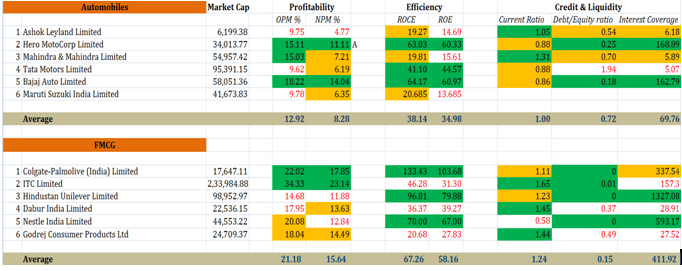

[II] Benchmark companies within the same industry/sector: Pay close attention to the average ratios of the sector in which the company operates.

The correct way of analyzing the company is to club together all the companies in a particular sector and then arriving at an average figure before rating each company based on how far or below they are from the industry average.

[III] Don’t go overboard with benchmarking: While a benchmark industry standard (i.e. arriving at an average figure for every industry) is good to some extent, it should be used with caution. The reason is simple, while evaluating and scoring companies we are comparing its historical performance which is at best an indication but not a guarantee of the future. Important point to note here: while comparing different companies in the same sector/industry, some companies may be in different growth phases / life cycles. Some may be start ups while others may be well established or in their growth phase. While they may operate in the same industry, it is important to give due consideration to their stage of business maturity.

[III] Don’t go overboard with benchmarking: While a benchmark industry standard (i.e. arriving at an average figure for every industry) is good to some extent, it should be used with caution. The reason is simple, while evaluating and scoring companies we are comparing its historical performance which is at best an indication but not a guarantee of the future. Important point to note here: while comparing different companies in the same sector/industry, some companies may be in different growth phases / life cycles. Some may be start ups while others may be well established or in their growth phase. While they may operate in the same industry, it is important to give due consideration to their stage of business maturity.

Benchmarking is an important method of analysis but it is important to consider factors like future prospects/outlook, potential of the company. RATIO ANALYSIS IS EFFECTIVE BUT IT CAN ONLY TELL YOU ABOUT PAST AND DOES NOT TELL YOU ABOUT THE FUTURE. Future performance may be materially different from past performance.

[IV] Uniformity of approach: Different companies follow different accounting policies. For this reason, presentation of accounts differs for companies. It is important to make certain adjustments in the presentation or reclassification of items in order to make a rational comparison. The goal should be to make the accounts of different companies consistent with each other so that you can make a meaningful comparison between the accounts. If the accounts themselves are not consistent or are not uniform, then the ratios derived from such accounts will also be distorted.

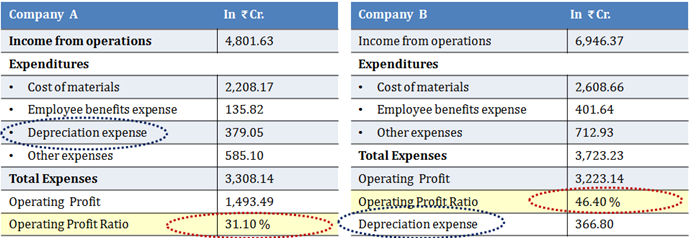

Example: some companies may report depreciation as part of total expenditure, while others may disclose it as a separate line item. Effectively this will have a material impact on the operating profit ratio.

In case of Company A – it reports depreciation as part of total expenses while in case of Company B – total expenses exclude depreciation. So operating profit margin of Company B will be much higher than the operating profit margin of Company A, purely because of the way these companies present their accounts.

[V] Read lots of financial statements: Understanding and calculating ratios is extremely simple but what will make you better as an investor is to read lots of financial statements. Often times you will see that it is easy to improve the appearance of a company’s financial statements for a given period and is mostly done towards the end of an accounting period (commonly referred to as creative accounting/ window dressing).

Example: a company may delay paying its suppliers for a while (for the raw material it used) in order to maintain a healthy cash balance for the end of a given period (i.e. quarter or financial year). Looking at financial statements and trends over a longer term can be helpful and give you valuable insights.

Similarly, following a particular company’s (or sector’s) accounts over a period of time will help you understand the trends in that sector. For example, in hospitality companies, if you track closely you will know that the 3rd quarter registers the highest revenue growth owing to December being a holiday season. Any bigger deviation from an average here could be (but may not always be) due to creative accounting.

[VI] Look beyond quantitative – MOST IMPORTANT: No matter how good the financials may be always look at qualitative aspects before investing. In fact, Management’s integrity, honesty and competence are some of the things you should look at even before getting interested in the financials of a company.

____________________________