This is the part 2 of – this article on ICDR Regulations

Let’s take the example of Confused Publicity Limited (“Issuer”). The Issuer is a media company primarily engaged in the business of writing about the lifestyle of the rich and famous and regularly features celebrity interviews in many of its magazines. Many of its clients are famous actors, cricketers, singers etc. The Issuer recently filed for its Initial Public Offer (“Issue”) and is hoping to raise money for the launch of its own television channel.

Daredevil Stuntman (“DS”), a world famous stuntman who has many accolades to his name is a regular feature in the magazine, “Of Mad People”, the most successful publication by the Issuer. DS has also signed an exclusive agency agreement with the Issuer to give a monthly interview for publication in the magazine, “Of Mad People” for 12 consecutive months.

Offer Document

The Issuer engages Sleepless and Working Associates (“SWA”) as the law firm for writing its SEBI Offer Document filing. While drafting, the SWA team led by Awesome Partner and Inquisitive Associates disclosed the following information about DS:

“The Company has exclusive interviewing rights for some of the most successful daredevils in the country including the very special DS, the world famous daredevil who recently broke multiple bones trying to walk down the escalator steps using his hands”.

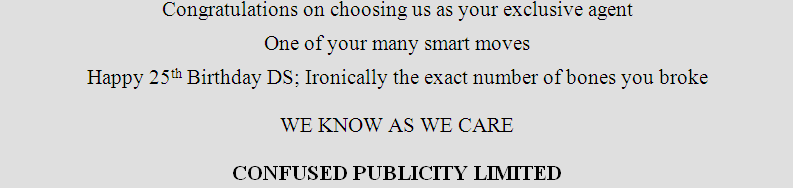

After filing the Offer Document with SEBI, the Issuer came out with the below advertisement (in regular course of business) in a popular national newspaper dated 25th February 2012:

The same afternoon, on which the advertisement got published, Crazy Valuations (“CV”), the lead manager to the Issue got a call from the dealing officer at SEBI (“Dealing Officer”). The Dealing Officer pointed to regulation 60 and claimed that the advertisement violated the publicity restrictions under the ICDR Regulation. Not sure of what to do, the CV team assured the Dealing Officer that they will look into the matter. CV team contacted the SWA team and asked for an opinion.

SWA team managed to find five disclosures in the advertisement which were “extraneous to the contents of the Offer Document”:

- CPL is the exclusive agent for DS

- DS’s birthday is on the 25th of February

- DS was born in the year 1987

- DS broke 25 bones

- CPL knows things because they care

Awesome partner got the entire SWA team together and arranged for a conference call with the Issuer. After all, these issues were really important for someone who may have long term investment plan in the company. After checking the disclosure language in the Offer Document, the SWA team concluded that;

With regard to item (1) – Appropriate disclosures have been made;

With regard to item (2) – DS’s birthday is not. At this point, the SWA team got worried; why was the advertisement not sent to them for approval prior to its release?

With regard to item (3) – DS’s year of birth is again not disclosed (the SWA team wondered whether that was not public information? After all, DS is the most famous daredevil in the country.

In any event, Regulation 60 (5) of the ICDR Regulations (stated above), makes sure that publicly available or not, the information must already be in the Offer Document filed with SEBI for it to be used as publicity.

With regard to item (4) – SWA team worried that while they had disclosed the incident relating to DS’s broken bones; the exact number of bones broken was not mentioned. Could this adversely affect the investors or the stock price post listing?

With regard to item (5) – Each of the Inquisitive Associate looked at each other, then down at the note and finally looked towards the Awesome Partner who looked outside his 17th floor office towards an advertising hoarding that read “Speechless I stood before this wonder ~ Egypt ~ where it all begins”. Next morning the Awesome Partner left for a Mediterranean vacation.

Some other publicity restrictions

The problem of what can and what cannot be disclosed is not the only one that makes life difficult for Issuers. Once it is determined that the information could be used as publicity or as advertisement material, the relevant advertisement must contain a statutory legend. As per sub-regulation 3 of Regulation 60,

“All public communications and publicity material issued or published in any media during the period commencing from the date of filing draft offer document with the Board till the date of allotment of securities offered in the issue, shall prominently disclose that:

- the issuer is proposing to make a public issue or rights issue of the specified securities and has filed a draft offer document with the Board or has filed the red herring prospectus or prospectus with the Registrar of Companies or the letter of offer with the designated stock exchange, as the case may be.

- the draft offer document, red herring prospectus, as the case may be, is available on the website of the Board, lead merchant bankers or lead book runners.

It goes without saying that the legend must be in a readable font size. Note also that explanation to Regulation 60 explains, Publicity material as “public communication or publicity material” includes corporate, product and issue advertisements of the issuer, interviews by its promoters, directors, duly authorized employees or representatives of the issuer, documentaries about the issuer or its promoters, periodical reports and press releases.

Some of the more common questions that are raised by the Issuer companies include questions such as; does a pamphlet require the legend? Or, should they post legends on internet advertisements? What about television advertisements? Advertisements already released for publication?

Some practical problems surface when you have to insert these legends on an advertisement which is so small that it could barely contain the contents of the publicity, a clipping on 1/4th of a web page for instance or one that is published in a fashion magazine which unlike most newspapers and educative magazines has such high readership that it’s hard to get even a 10 line space on the page.

My favorite is the press invitation sent to journalists a few days before the opening of the issue. The invitation reads something like this “…you are cordially invited to a presentation on the upcoming initial public offering of Confused Publicity Limited of [X] shares in a price band of [Y-Z]….”

Should the invitation card of a five square inch dimension, then have a legend restating the exact same thing as the invitation itself to satisfy the requirements of Regulation 60 (3)? I don’t know the answer to that. Does such an invitation constitute publicity at all? What about if the Issuer company places a signboard on its corporate office building containing its name and advertising slogan?