When to use: Short Call Condor Option Strategy is similar to a short call butterfly spread strategy. This Strategy is implemented when the investor believes that the stock is going to break out of a trading range in the near future but is not sure in which direction.

How it works: Short call condor strategy uses four option contracts with the same expiry date but with different strike prices. In this strategy, the investor sells/writes 1 in-the-money call option and 1 out-of-the-money call option; and buys 1 in-the-money call option and 1 out-of-the-money call option, each with the same expiry date, T.

For example: On 4th September 2013, when the share of Hindustan Unilever Limited was trading at Rs. 616.50, you decided to sell/write 1 in-the-money call option at a premium of Rs. 42.75 with a strike price of Rs. 580.00 expiring 26th September 2013; sell/write 1 out-of-the-money call option at a premium of Rs. 6.50 with a strike price of Rs. 660.00; bought 1 in-the-money call option at a premium of Rs. 31.55, with a strike price of Rs. 600.00; bought 1 out-of-the-money call option at a premium of Rs. 12.65, with a strike price of Rs. 640.00.

For Short Call Options: If the price of Hindustan Unilever Limited share stays below Rs. 580 and/or Rs. 660 (i.e. the strike price of the 2 short call options) until expiry, you will retain the the entire (or partial) premium amount (depending upon where the price of the share settles). If however the price rises above Rs. 580 and/or Rs. 660, the buyer of the call option may exercise his option and make a profit based on how far above does the stock price rise. From the perspective of the seller of the call (you), you will start suffering a loss once the stock price rises above Rs. 635.75 (i.e. lower strike price + total premium received on the two short call options).

For Long Call Options: If the price of Hindustan Unilever Limited rises above Rs. 600 and/or Rs. 640 (i.e. the respective strike prices for the 2 long call options), you can exercise your respective option, but the price of the stock must rises above Rs. 644.20 (i.e. lower strike price + total premium paid on the two long call options) for you to exercise your option and make a profit.

Risk/Reward: In short call condor strategy, the maximum risk is limited and occurrs when the stock closes either below the lower breakeven point or above the upper breakeven point and the maximum reward/profit is also limited and will be realized when the stock closes on either side of the upper or lower strike price on expiry.

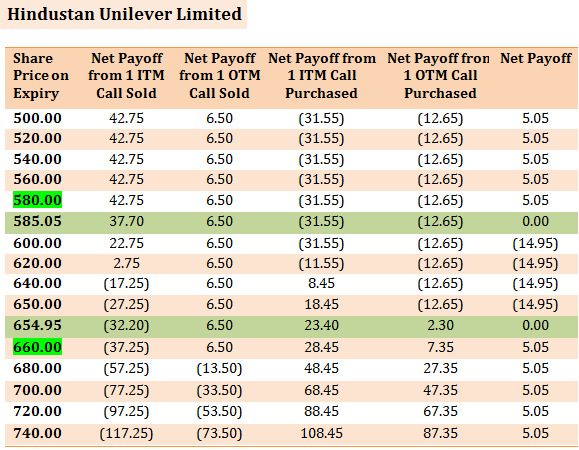

The table below clarifies the above points and shows the net payoff of short call condor option strategy assuming different spot prices on the expiry date:

The table above allows you to easily see the break-even points, maximum profit and the loss potential on expiry in rupee terms. The calculations are presented below.

The two break-even points occur when the price of the underlying share equals Rs. 585.05 and Rs. 654.95.

First Break-even Point = Lowest Strike price + net premium paid = Rs. 585.05 (580 + 5.05)

Second Break-even Point = Highest Strike price – net premium paid = Rs. 654.95 (660 – 5.05)

The maximum profit is equal to the net premium received (i.e. Rs. 5.05). It will be made if the underlying share price upon expiry is on either side of the upper or lower strike prices i.e. Rs. 580 or Rs. 660.

The maximum loss which the investor may suffer equals Rs. 14.95. Maximum loss, in this example, will be incurred if the share price falls below Rs. 585.05 or rises above Rs. 654.95 on the expiry date.

How to use the Short Call Condor Option Strategy Excel calculator

Just enter your expected spot price on expiry, option strike price and the amount of premium, to estimate your net pay-off from the Strategy.

Note: The example and calculations are based assuming a single share though in reality options are based on lots of many shares. For example Hindustan Unilever Limited call option contract is for 500 shares. Accordingly the net premium received will be Rs. 2,525.00 for 4 lots (i.e. 5.05*500) in our example.

Also Note: Unlike the buyer of an option who only pays the premium to buy the option, the seller of an option must deposit a margin amount with the exchange. This is because he takes an unlimited risk as the stock price may rise to any level. In case the price rises sharply above the strike price, the exchange utilises the margin amount to make good the profit which the option buyer makes. The amount of margin is decided by the exchange and it typically ranges from 15 % to 60 % based on the volatility in the underlying stock and market conditions. In the above example, as a seller of call option, you will have to deposit a margin of Rs. 87,420.00 (i.e. Strike price * Lot size * 14.10%) for selling/writing 2 lots of Hindustan Unilever Limited call option. Note that the total value of your outstanding position in this case will be Rs. 6,20,000 (i.e. strike price * lot size).