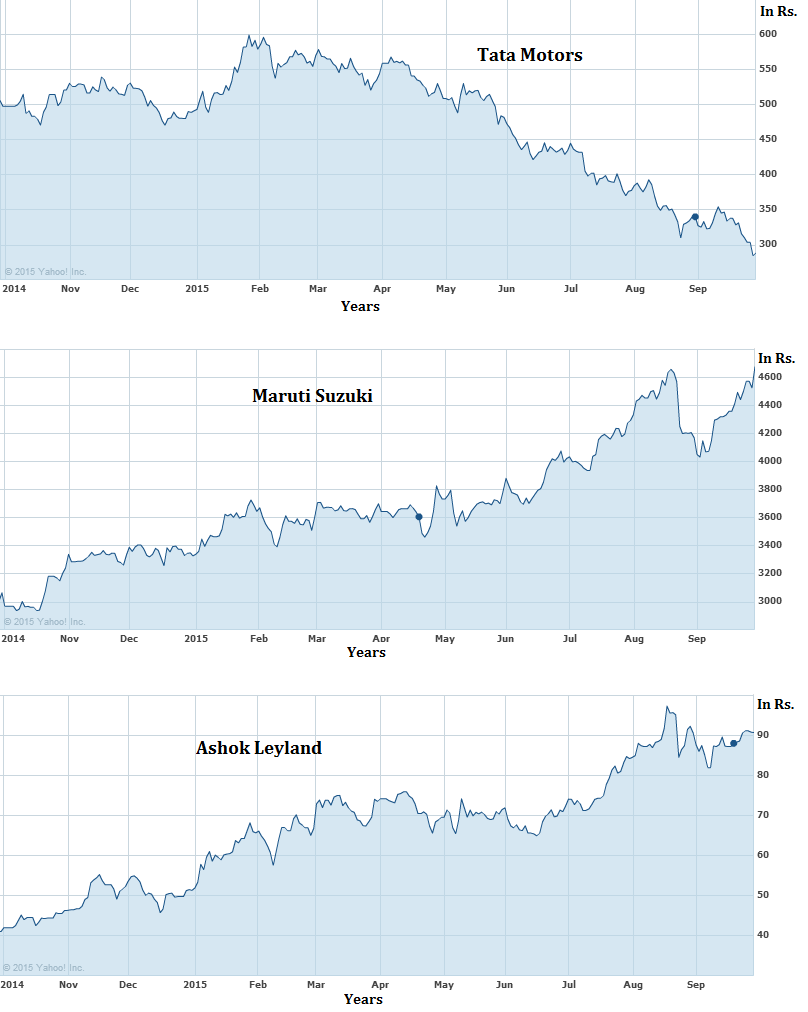

Over the past one year, Tata Motors has fallen over 42% (from Rs. 505.34 to Rs. 288.65), on the other hand its competitor, Ashok Leyland in the medium & heavy commercial vehicles (M&HCV) has surged 120.02 % (from Rs. 41.20 to Rs. 90.65) and Maruti Suzuki, its biggest competitor in passenger vehicle segment has rallied 55.38% (from Rs. 3008.60 to Rs. 4674.75).

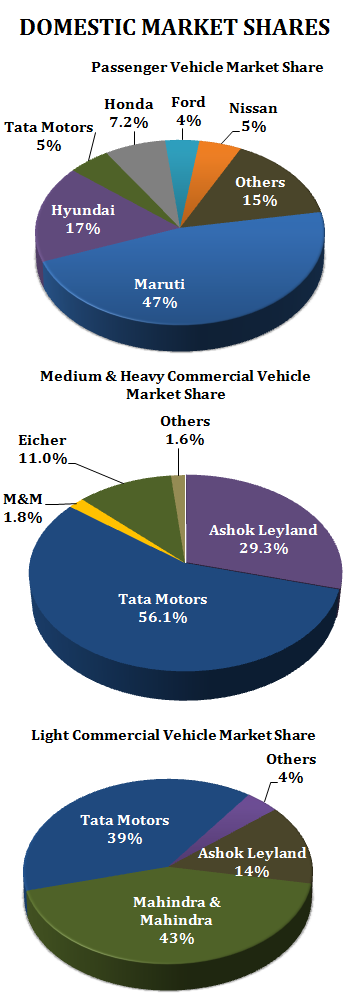

In Q1 of FY 2016, Ashok Leyland’s market share in M&HCV segment rose to 29.2% (from 24.6% in Q1 of FY 2015). On the contrary, its close competitor and market leader, Tata Motors lost its market share from 57.9% to 56.3%.

Ashok Leyland’s improved performance was mainly on account of diversification of business into (i) Core business which includes trucks and buses and (ii) Non-core businesses which includes defence, engines and power solutions, Light Commercial Vehicle (LCV) under the brand name DOST, spare parts and construction equipment.

- M&HCV business witnessed a 16.5% growth in FY 2015.

- The LCV segment has lost market share from 62% in FY 2008 to only 39% in FY 2015. This was on account of increased competition mainly from Mahindra & Mahindra and Ashok Leyland.

- The passenger vehicle segment operated at capacity utilization of only 25 % in FY 2015. In this segment, Tata Motors faces tough competition from Maruti.

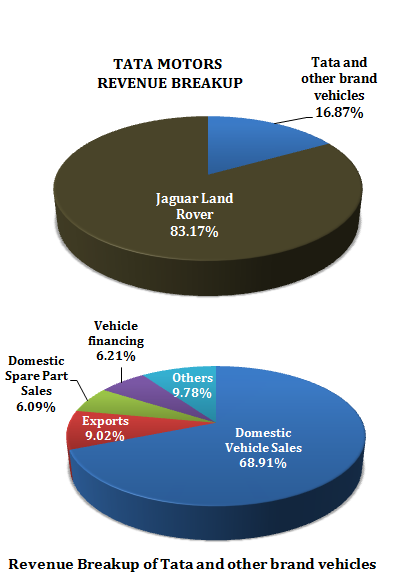

- Even in domestic passenger vehicle segment, major revenue comes from the sale of Jaguar Land Rover (JLR) vehicles.

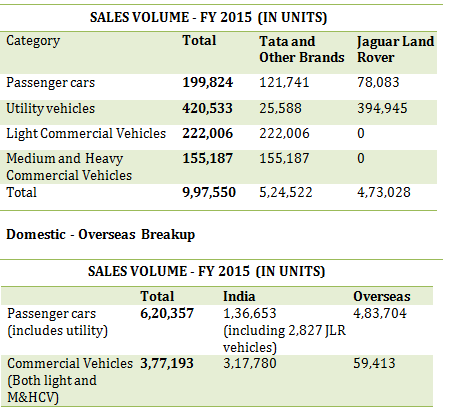

- Domestic vs. Export Performance:

Passenger Vehicle: Domestic sale volume – 22% | Exports – 78%

Commercial Vehicles: Domestic sale volume – 84% | Exports – 16%

WHY IS TATA MOTORS STOCK PRICE FALLING

Tata Motors – It should really be Jaguar Land Rover (JLR) Motors

Tata Motors operates in 2 business segments – Automotive Operations and Others

[1] Automotive operations accounted for 99.5% of the total revenues in FY 2015. The Company’s automotive operations segment is further divided into Tata and other brand vehicles (including vehicle financing) and Jaguar Land Rover.

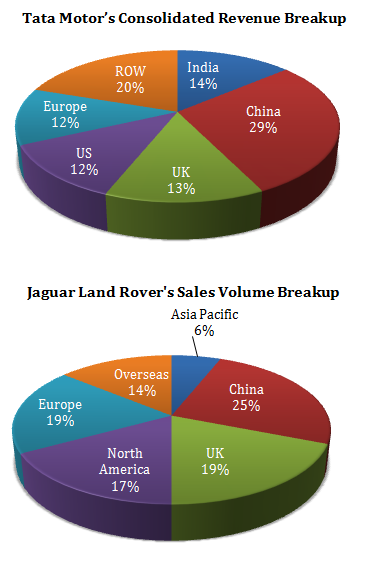

Jaguar Land Rover contributed 83.2% of the Company’s total automotive revenue and only the remaining 16.8% came from Tata and other brand vehicles.

[2] Others – The other operations business segment includes information technology, machine tools and factory automation solutions.

Clearly, Tata Motors is largely being driven by JLR sales and company’s Indian operations have been a drain on its financials.

| FINANCIAL PERFORMANCE | ||

| Tata Motors Standalone | Jaguar Land Rover | |

| (In Rs. Cr.) | FY 2015 | FY 2015 |

| Net Revenue | 39,524 | 2,02,848 |

| EBITDA | (800) | 38,332 |

| EBITDA % | (2.2) | 19% |

| PBT | (3,975) | 24,250 |

| PAT | (4,739) | 18,906 |

| Conversion exchange rates for above data: 1 USD = 62.50 INR; 1 GBP = 1.4843 USD | ||

The Impact of China Slowdown on Tata Motors

The Impact of China Slowdown on Tata Motors

China is JLR’s single largest market, contributing over 25% to its total sales volume (for FY 2015). China has been the key growth driver for JLR where it has increased its market share from 4.5% to 8.6% between FY 2011 and FY 2015. Other major players in Chinese premium and luxury car market include Audi, BMW and Mercedez.

In FY 2015, luxury car market in China grew at 7%, as compared to 20% in 2014. The demand slowdown in China has adversely impacted the sale of JLR cars which has decreased 33.4% (i.e. from 32,912 units in Q1 of FY 2015 to 21,920 units in Q1 of FY 2016.

Non-macro issues (China specific) – Pricing strategy of the locally assembled Range Rover Evoque (SUV) model – In China, JLR has begun the local production of its Range Rover Evoque SUV (in a JV with domestic car maker Chery). This was highly criticized by the Chinese buyers as it was only 5% lower than the price of the imported version. Another issue was that buyers were not happy with the Chery logo on the locally produced Evoque and also feared that the quality of the product might be inferior to the imported model. All this contributed to bad sales performance for JLR in its largest market.

OUR VIEW

While what will obviously work very well for Tata Motors is a pickup in global economy, particularly China. That said, if Tata Motors manages to increase its market share from the current 14% in the domestic market; that could be an added boost which is possibly getting missed out in major analyst reports. It is true that Chinese economy has slowed down, its impact on the sale of luxury cars is clearly exaggerated. There is no reason why Tata Motors stock should trade at current levels. In our view this is mostly on account of aggressive selling by traders and the stock price should adjust going forward.

For pure value investors, Tata Motors at 288 is a screaming buy!

As Warren Buffet said, “Great investment opportunities come around when excellent companies are surrounded by unusual circumstances that cause the stock to be misapprised.”

* References:

[1] Tata Motors Annual Reports (various years)

[4] JLR Annual Report for 2015

[2] Society of Indian Automobile Manufacturers (SIAM)

[3] China Association of Automobile Manufacturers (CAAM)

Again very good analysis Mr Rajat Sharma… Fully agree but I thought we should factor in the domestic biz as well, even though it is small pie (Currently)

The point is – per above data (dint verify but should be right!) : As of FY15, Domestic Biz of TAMO is about 40K crore Approx in Revenues and is deep in red with 4K crore loss. But this is a very cyclical biz and right now in trough and getting out. HCV demand in India is very cyclical/periodic and related to rate environment. And all indications are that we are slowly moving to lower rates and with a lag effect should boost domestic CV demand in 18 months. So good chance that by FY18 we have a 50-55K Domestic revenues and 20%+ Profit margins, that alone could boost TAMO’s MCap by 100% from present lows, so is a win win situation i felt. (Crude Guesses only, am just a interested investor BTW)

The other point to watch is the diesel emission norms in India (Euro 5 etc), don’t think much investment needed on this ( think it is refiners who must invest to produce the right grade fuel) but this can trigger demand esp if it is enforced by govt demanding phaseout of old CVs in a time frame.

Cant agree more Sir, totally a buyer in this script. Imagine a global MNC and a trusted brand like Tata’s trading at 1.2X sales. Most importantly the leadership status it has itself needs better P/E valuation and last of all is the DCF value, it stands at around 700 for me