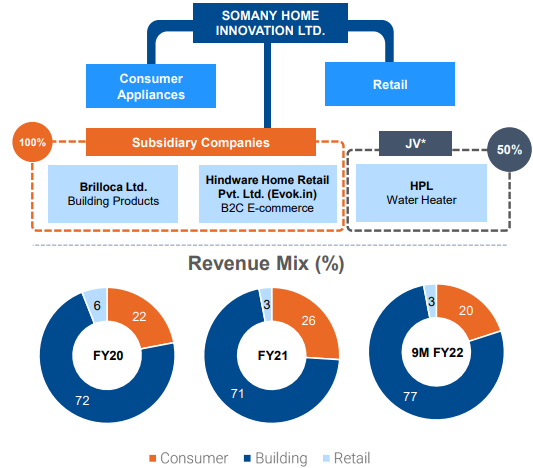

Somany Home Innovation Ltd (“SHIL” or the “Company”) is the fastest growing player in Consumer Appliances and the leader in the Building Product segment with 3 distinct distribution channels to market. The Company is focused on servicing end-consumers and involved in branding, marketing, sales & distribution and service of various product categories.

The Company houses the Consumer Appliance business and offers a range of innovative products across kitchen appliances, sinks, air coolers, water purifiers, and ceiling and pedestal fans categories. It has a presence in the kitchen and furniture fittings segment in collaboration with the Italian company, Formenti & Giovenzana under the brand ‘FGV Powered by Hindware’.

Somany Home Innovation offers furniture and interior products under the brand ‘EVOK by hindware’. It offers a versatile range of best-in-class sanitaryware, faucets, plastic pipes and fittings, overhead water storage tanks, column pipes, and premium tiles housed under Brilloca Limited, a wholly-owned subsidiary of SHIL. Somany Home Innovation has entered into a joint venture with Groupe Atlantic of France to further leverage the opportunities in fast-growing Consumer Water and Electrical Heating segment in India under Hintastica Private Limited (HPL).

Financial Performance

| Particulars | FY19 | FY20 | FY21 |

| Revenue (In Rs. Cr.) | 1,670.87 | 1,613.12 | 1,775.21 |

| Growth | – | -3.46% | 10.05% |

| EBITDA (In Rs. Cr.) | 124.21 | 88.15 | 143.10 |

| EBITDA Margin | 7.43% | 5.46% | 8.06% |

| EBIT (In Rs. Cr.) | 104.52 | 42.16 | 103.83 |

| EBIT Margin | 6.26% | 2.61% | 5.85% |

| PBT (In Rs. Cr.) | 84.81 | 33.17 | 92.41 |

| PAT (In Rs. Cr.) | 54.70 | 23.11 | 54.84 |

| PAT Margin | 3.27% | 1.43% | 3.09% |

| EPS (In Rs.) | 7.57 | 3.20 | 7.59 |

| EPS Growth Rate | – | -57.75% | 137.30% |

| Historic P/E (Closing Price of 31st March) | – | 22.81 | 35.23 |

| CURRENT P/E | 15.09 | ||

| CURRENT PE/ROE | 0.91 | ||

| D/E | 1.25 | 1.19 | 0.56 |

| PE/ROE | – | 2.71 | 2.12 |

| EV/Sales | 0.77 | 1.52 | 1.69 |

| Interest Coverage | 4.36 | 2.65 | 4.85 |

| ROCE | 22.80% | 14.70% | 27.82% |

| ROE | 22.59% | 8.43% | 16.62% |

Quarterly Performance

| Quarterly Results | Q3 FY 2021 | Q4 FY 2021 | Q1 FY 2022 | Q2 FY 2022 | Q3 FY 2022 | TTM | Q-o-Q % | Y-o-Y % |

| Revenue (In Rs. Cr.) | 551.37 | 613.30 | 342.30 | 616.69 | 649.01 | 2,221.30 | 5.24% | 17.71% |

| EBITDA (In Rs. Cr.) | 55.59 | 64.60 | 10.48 | 49.48 | 53.18 | 177.74 | 7.48% | -4.34% |

| EBITDA Margin | 10.08% | 10.53% | 3.06% | 8.02% | 8.19% | 8.00% | ||

| PAT (In Rs. Cr.) | 37.66 | 22.26 | 103.63 | 24.88 | 35.86 | 186.63 | 44.13% | -4.78% |

| PAT Margin | 6.83% | 3.63% | 30.27% | 4.03% | 5.53% | 8.40% | ||

| EPS (Rs.) | 5.21 | 3.08 | 14.33 | 3.44 | 4.96 | 25.81 | 44.19% | -4.80% |

Q1 FY 2022 – Exceptional items comprising recognition of gains of Rs. 66.11 Cr. from its investment in Hintastica Private Limited on account of loss of control of subsidiary and gain of Rs. 34.75 Cr. on account of slump sale of water heater business undertaking by the Company to Hintastica Private Limited.

Q3 FY 2022 Highlights

- Building Products Business Update – Stellar growth witnessed. Revenue grew by 32% Y-o-Y to ₹496.3 Cr. Demand is supported by customers going for home improvement and growth of real estate sector owing to low-interest rates, Government incentives, and increasing sales. Hindware recorded significant rise in both Sanitaryware and Faucets market shares on the back of product and design leadership, brand salience, wide product portfolio, and distribution network. Strengthened the retail and distribution network to bolster presence in tier 1 & 2 markets and reach out to tier 3-5 markets. Launched Aspiro range of Sanitaryware and faucets which is seeing great traction in the market

- Plastic Pipes & Fittings Update – TRUFLO registered a growth of 33% Y-o-Y to report sales of ₹155.6 Cr. TRUFLO grew in sales, volumes and market share owing to the wide acceptance of the brand and quality of the products. The business recorded a favorable mix of product sales, with the CPVC range contributing significantly to the overall realization.

- Consumer Appliance Business Update – Growth in revenue but profitability was impacted on account of significantly higher input costs and slow market demand. Revenue for the quarter stood at ₹130.9 Cr., growing by 7% Y-o-Y. Appointed 93 new distributors to capture growing consumer demand Launched 16 new exclusive kitchen galleries (140 total pan-India) during the quarter to be available to customers through as many touchpoints as possible. 19 new launches across product categories in Q3 FY22 to expand product range

- Retail Business Update – Increased demand for home renovations led to growth in revenue and profitability. Revenue stood at ₹21.8 Cr., growing by 23% Y-o-Y. Launched ~200 new products to expand the product portfolio to offer variety across price points. Added 10 new EVOK Franchise stores to strengthen omnichannel presence

INVESTMENT RATIONALE

Expanding Horizons to Unlock Value

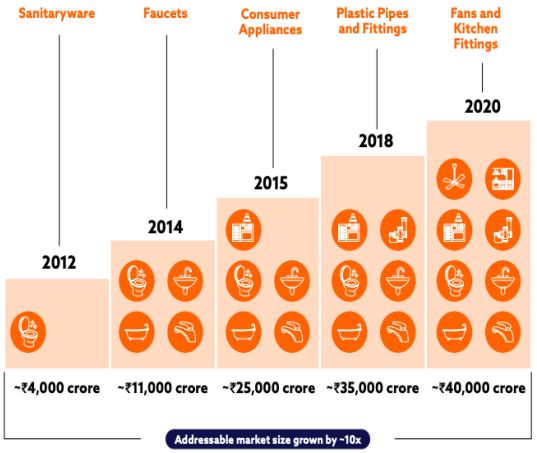

From being present only in the sanitaryware business segment over a decade ago, the Company, over the years, has expanded into numerous customer-facing businesses. This has helped it to grow its addressable market size by ~10x. In each of its businesses, the Company has built capabilities that have helped it position ourselves among the top 5 players within the first five years of entry in that segment. This has de-risked the business from dependence on a single product segment.

Consumer Appliance | Guidance on Revenue growth and Margin Expansion

Somany Home Innovation is #2 player in Kitchen Chimneys, #5 player in Air coolers and #6 player in water heater segment. Kitchen appliances are 45-48%, while air coolers and water heaters are 15-20% each of segment sales. The product portfolio consists of household appliances – from kitchen appliances, such as kitchen chimneys, cooker hoods, built-in hobs, cooktops, built-in ovens, sinks, through the brand Hindware Kitchen Ensemble; to storage, instant and gas water heaters through Hindware Atlantic; to water purifiers and air purifiers through Moonbow by Hindware and Hindware; and to air coolers and ceiling fans through Hindware Snowcrest ¡ It recently forayed into the furniture and kitchen fittings segment, through a strategic marketing tie-up with Formenti & Giovenzana, under brand FGV powered by Hindware. The Management has guided for this segment to do revenues of Rs. 1300- Rs. 1500 Cr. by FY25-26 which broadly translates to ~30% FY21 to FY25 CAGR.

Leadership Position in Sanitaryware

The strong product portfolio, robust brand recall for Hindware and wide distribution network have led to continue its leadership position in sanitaryware (Hindware has >60-65% market share) and faucets segment (Hindware is one of the leaders). Building Products (ex-pipes) posted revenues of Rs. 861 Cr. FY21 on account of covid related disruptions in H1FY21. The Sanitary ware and Faucets business is largely mature, however as the segment is incubating the tiles, pipes and fittings business, the margins are currently on the lower end. The Management has guided for the segment to comfortably achieve 14-16% EBITDA margins by FY25-26. On the revenue side, the management guidance stands at 1.3-1.5x of industry growth which broadly translates to ~11% CAGR.

The Company’s home interior products business under the brand ‘EVOK by hindware’ consists of a range of products such as furniture, modular kitchen, decor, and furnishing categories. It has 2 owned stores and 29 franchise. Over the years, the Company has significantly reduced its owned stores to reduce its overheads and improve its overall margins. Thus focusing more on franchise led operations and ecommerce business.

INVESTMENT CONCERNS

Raw Material Prices

Given increase in input prices including brass (Faucets), Gas Prices, Polypropylene (Sanitary ware) directly impact the contribution margins. Though the Company has already take price hikes (~10% in Faucets and ~16% in Sanitary ware) and intend to take few more in coming quarters. Any further hikes may impact the margins directly.

Slower Ramp-Up of Consumer and Pipes Division

Overall investment thesis of growth and margin expansion will be significantly impacted if the ramp-up in consumer and pipes division is slower than expected.

Working Capital Management

It continues to remains a working capital heavy business (~110 days cycle).

Linkages to cyclical real estate sector and presence in a competitive industry.