Amara Raja Batteries Limited (“Amara Raja” or the “Company) is the second largest manufacturer of lead-acid storage batteries for industrial and automotive applications in India. The Company’s products are supplied to various user segments viz., telecom, railways, power control and UPS under Industrial Battery business; and to automobile OEMs, replacement market under Automotive Battery business. Amara Raja’s products are being exported to various countries in the Indian Ocean Rim. The Company also provides installation and maintenance services to customers. Leading automotive and industrial battery brands of the Company are Amaron, PowerZone, Power Stack, AmaronVolt and Quanta.

WHAT’S DRIVING THE STOCK

Competitive Advantage in the Indian Battery Market

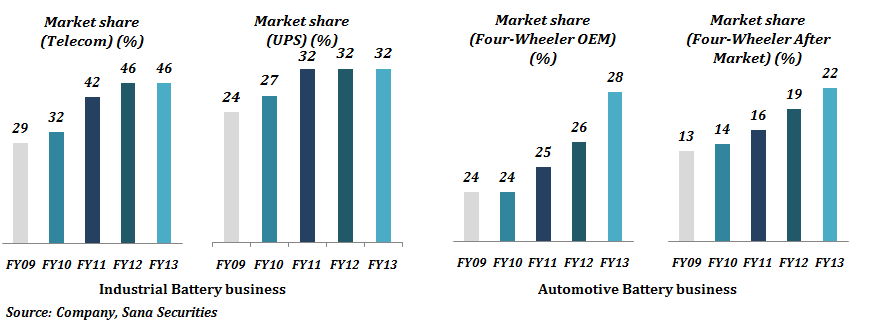

Exide and Amara Raja control 90 % of the organized Indian Battery Market.

Amara Raja’s market share in different segments: 4-wheeler (OEM-28 %, Replacement -37 %), 2-wheeler (Replacement – 25 %), UPS (32 %) and Telecom (46 %). Amara Raja enjoys strong brand equity with flagship brands like Amaron and PowerZone targeting the urban and rural markets, respectively.

The Company’s recent foray in the two wheeler Original Equipment Manufacturing (OEM) segment is expected to boost volumes and help expand its market share in the 2 wheeler segment as it currently caters to only the replacement market.

The Company derives about 60 % of its revenues from the auto segment, where it has Ford, Maruti, Hyundai, Honda, Mahindra & Mahindra, Tata Motors, and Tafe as its clients. The industrial division, in which the company primarily makes telecom and UPS batteries, brings in the rest of the revenues. The Company enjoys competitive advantage in the automotive battery division due to the 100 % share of business with Ford India and Daimler Benz; 100 % share of business in Maruti AStar exports and Hyundai ‘EON’. Amara Raja is also the first supplier of batteries to M&M for Scorpio Micro Hybrid vehicles. In the industrial battery business, Amara Raja’s alliance with Bharti Airtel generates large exports to Africa, Sri Lanka and Bangladesh.

Despite the slowdown in the Indian automobile industry, ARBL’s net profit was up at Rs. 286.7 Cr. versus Rs.215.1 Cr. (i.e. a 33 % year on year growth). For the same period, the net sales were up at Rs. 2,961.40 Cr. versus Rs.2,364.5 Cr. (i.e. a 25 % year on year growth). For the nine month period ended December 2013, the Company reported net sales of Rs. 2,552 Cr. and net profit of Rs. 287.39 Cr. This growth is attributed mainly to a significant volume growth of 19 % in automotive four-wheeler batteries, 26 % in automotive two-wheeler batteries and 14% in industrial batteries. The pan-India consumer response to Amaron and PowerZone branded home UPS products has been very promising during FY 2013.

Strong replacement (after) market

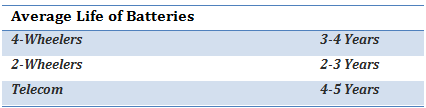

The Company is a dominant player in the aftermarket segment for four-wheeler and two-wheeler batteries. Despite a slowdown in new vehicle sales, the Company remains better off as it has a huge market for replacing old batteries in existing vehicles. The average life span of battery ranges from 2-4 years and since the battery replacement decision cannot be delayed, companies like Amara Raja are expected to benefit immensely from the ever increasing number of registered vehicles on Indian roads. Auto sales between 2009 and 2013, implies that the replacement demand for vehicles sold during this time will increase over the next few quarters. The Company generates three-fourths of its auto segment revenues from the replacement markets. The Company has a market share of 35 % and 25 % respectively in the replacement markets for cars and two-wheelers. We expect strong replacement demand over FY 2014-2016 and the Company is expected to grow above the industry average during this period.

Extensive distribution network and Capacity Expansion

Amara Raja’s, distribution network plays a vital role in aftermarket automotive batteries sales and Amara Raja has been successful in creating a dominant network (287 franchised distributors, including 21,000 retailers and 400 plus service hubs-second largest in the Indian Battery Market). The Company’s PowerZone network comprises of 1,100 exclusive retail partners spread across semi-urban and rural locations. The Company plans to double its distribution network within the next 2-3 years and will focus more on areas where unorganized players are predominant – i.e. semi urban & rural areas.

Amara Raja’s, distribution network plays a vital role in aftermarket automotive batteries sales and Amara Raja has been successful in creating a dominant network (287 franchised distributors, including 21,000 retailers and 400 plus service hubs-second largest in the Indian Battery Market). The Company’s PowerZone network comprises of 1,100 exclusive retail partners spread across semi-urban and rural locations. The Company plans to double its distribution network within the next 2-3 years and will focus more on areas where unorganized players are predominant – i.e. semi urban & rural areas.

Sale of Quanta branded batteries has also increased with AQUA (distribution channel for Quanta brand) stores increasing from 75 to 100 in FY 2013. In Industrial battery division, the Company is planning to invest Rs. 4.40 billion to augment capacities in Large VRLA and automotive 4-wheeler product lines over FY2014-15. This investment is in addition to the already approved capital investment of Rs. 3.04 billion to expand capacities in Medium VRLA, automotive 4-wheeler and automotive 2-wheeler product lines.

UPS segment sales to rise with increasing power demand-supply gap

India’s increasing power deficit (about 10-12% average) is the critical factor driving growth of the home UPS industry. While untapped rural and semi-urban markets hold big potential, the urban market continues to provide an equal opportunity due to the persisting power demand-supply gap. Frequent power shortages provide a huge market opportunity for the Company’s industrial battery segment for home UPS batteries in future. The demand will mostly come from the southern markets including Tamil Nadu, Karnataka and Andhra Pradesh with the power supplies going off track there. Indian UPS market is estimated to be US$ 3-3.5 billion.

WHAT’S DRAGGING THE STOCK

Volatility in Lead prices | Concerns around Inflation

Sharp increase in raw material prices has been a key concern. In FY 2013, raw material prices showed an increasing trend. A sharp rise in lead prices which accounts for 85 % of the total raw material cost for the company has put pressure on margins. Increase in raw material prices had an adverse impact on the Company’s profits and margins. Further, Amara Raja source 45 % of lead via imports and hence a depreciating rupee is also a concern for the Company.

Increasing level of inflation will lead to a further rise in the Company’s cost of production and are likely to result in price hikes. Such price hikes will directly impact demand in the current subdued economic environment.

Weak Telecom Outlook

For FY 2013, the Company derived 20 % of its revenue from the telecom sector. Amara Raja’s revenue stream from telecom batteries has been hit on account of spectrum pricing issues, hurdles in network expansion and telecom companies resorting to cost cutting measures such as sharing of towers, thus bringing down the expansion of telecom infrastructure. Any further deterioration in the telecom industry will have a significant impact on Amara Raja’s industrial batteries division.

Slowdown in economy (sectoral impact)

During FY 2013, automobile sector witnessed a sustained slowdown on account of higher interest rates, rising fuel prices and declining consumption growth. Automotive Batteries contributes 60% to Amara Raja’s revenue. Further slowdown in the automobile sector could disrupt company’s growth prospects. For more on the outlook of the automobile sector visit – Indian Automobile Industry.

________________________

** The stock analysis of Amara Raja Batteries Limited including the financial report linked above, is for informational purpose only. This analysis should not be taken as a buy/sell recommendation. The circumstances of the company and the economic environment may have changed since the date of this stock analysis.

In world market there is tough competition between companies and sale of battery depends battery backup, price, and maintenance cost.