United Phosphorus Limited (UPL) is engaged in the business of manufacturing and sale of crop protection products, intermediates, speciality chemicals and other industrial chemicals. The Company offers a range of products including insecticides, fungicides, herbicides, fumigants and has established a broad product line that caters to the crop protection needs of a plant during all stages of its growth.

Fair Value Based on Price Earnings (P/E) – It is easy to calculate the Price Earnings Ratio of any stock by simply dividing its current price by its reported EPS of the last 4 quarters (take consolidated EPS). The best way to assess the PE is by comparing it to industry PE and with the historic PE for that specific stock.

Also see: Quantitative Analysis of United Phosphorus Limited Here.

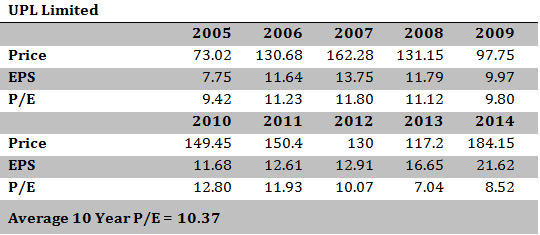

At the current price of Rs. 345 (closing price for – 13 January 2015), UPL’s trailing 12 month PE comes to 14.4 which is a 39% premium to its 10 year average PE Multiple of 10.37. The fair value of this stock, based on its 10 year historic PE multiple should be Rs. 248.5, while you will have to pay Rs. 345 for each share. Of course this may be over simplistic and does not factor in the future growth plans of the company. That said you will have to factor in significant change to justify buying the stock at current valuations.

At these prices and based purely on a PE analysis, UPL Limited is OVERBOUGHT. The stock has run up substantially over the last 52 week period. While the company is fundamentally sound and shows good prospects for future, I would stay away from this stock for now and try to enter it between 290-310 levels.

Positives for the Stock

Strong Financial Position

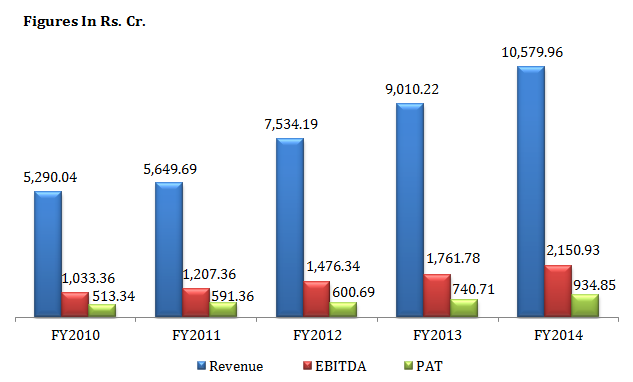

UPL has shown consistent growth over the last 5 years (i.e. 2010-11 to 2013-14). Its net revenue from operations over this period grew at an impressive CAGR of 17.88 %. For FY 2014, income from operations increased by 17.14 % to Rs. 10,770.88 Cr. from Rs. 9,194.52 Cr. and EBITDA increased by 22 % to Rs. 2,019.58 Cr. from Rs. 1,661.83 Cr. UPL has reserves in excess of Rs. 5,161.70 Cr. The Company has plans to cut gross debt by Rs. 5 billion in FY15E on the back of robust cash flow.

Dominant Market Position

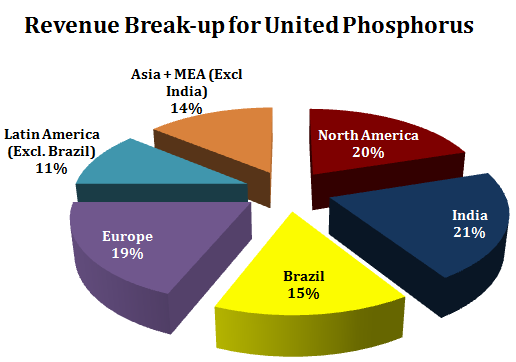

UPL enjoys a leadership position in the Indian crop protection market with 13% market share and with sales presence in over 120 countries. UPL is the twelfth largest agrochemical company in the world and the sixth largest generic agrochemical company. United Phosphorus has its operations in 124 countries through 28 manufacturing facilities and services consumers in 65 countries.

In order to further strengthen its position, the Company plans to launch 75-80 products in coming years.

Given the geographical diversification and its low-cost base, we believe that UPL enjoys an edge over competition and is placed well to leverage the upcoming opportunities in the global agrochemical space.

Investment Concerns

Demand concerns due to cyclical and seasonal effects

The agro-chemical industry, in general, is cyclical in nature with demand for some products staying variable. Seasonal usage follows varying agricultural seasonal patterns, weather conditions and pest related pressures. This volatility impacts the overall demand for agro chemicals. However, this seasonality risk is mitigated to a certain extent for UPL, given its geographic reach.

Volatility in input prices and company’s limited ability to pass on costs

The Company operates under the concept of ‘pass-through’, where lower raw material costs benefits are passed on to consumers as lower prices and vice versa. High volatility in prices of raw materials for agro chemicals, leads to lower price realization for the company and can cause margin pressures given that the average holding period of inventory is 3-4 months.

I just came across your site Rajat. I have been reading up on most of your articles since yesterday.

I am a total newbie to valuations. I have a (probably basic) question. How did you arrive at the fair value of 248.5 for UPL?

Thanks for taking the time to write these informative posts.

Look at this post where I explained this in detail – http://www.blog.sanasecurities.com/simple-rule-to-check-fair-value-of-stock/

Thanks..

So it is basically (current price * average PE)/ trailing PE!

Sure.

But this doesn’t capture the future growth or improvement. For a turnaround story, if they are on the verge of getting past their bad times, this won’t fit. Also, how do you assess loss making but soon to turnaround companies with huge potential like international paper since pe is not meaningful there. Will be great help if you could replu

You are right. Exactly.

If you see the linked post that’s what I said in there. Numbers are always historic and at best they suggest – “how things could go if nothing much changes”. Now – if a company is implementing new plans, launching new products, targeting exponential growth, surely you should factor all of that in when giving it a future multiple. I will try to put out another company’s report and cover this point in there 🙂

“At the current price of Rs. 345 (closing price for – 13 January 2015), UPL’s trailing 12 month PE comes to 14.4”-

I did not understand the calculation- EPS for 2014 is 21.62 as per your table.

So, PE is 345/21.62= 15.96, but you mentioned it as 14.4; How? Am I wrong?

No Rajeevan, you are not wrong. But this is why the numbers are not matching up – Trailing 12 month EPS is the EPS for the last 4 quarters. What you are reading is the annual EPS for the previous year. Look for EPS of past 4 quarters which is December 2014 – December 2013 in this case. they are not mentioned in this report (I must have taken them from quarterly numbers to keep things more accurate). Anyways these numbers are – 3.88, 6.73, 8.34, 5.02. This comes to 23.97. Now do the math.

Also – always nice to see people reading in details. Hope you got this now.