Fortunate are those who never studied the relation between stock prices and corporate earnings. Anybody who did would certainly have missed out on this year’s stock market rally. The purpose of writing this article is to analyse what led to the market rally followed by this week’s sell-off, and to present a stock market outlook for the coming weeks.

First, what led to increase in stock prices since the beginning of 2019?

For whatever reason, it was near certain that the current government was coming back to power with an even stronger majority than it did in 2014. Stock markets thrive on certainty and continuity. Irrespective of which government takes office, there is a certain degree of favoritism in how it awards projects and approves business plans. When there is a change in government, a lot of existing projects and a lot of ongoing plans get stuck as the new dispensation surely prefers to cancel these and award them to business houses closer to it.

Voting has completed on 80% of seats (424/542) for general elections of 2019. Going by rumours and unverified sources, it seems that the current government may fall short of the majority mark. While it is largely expected that Modi government is coming back to power, it may not do so with the kind of majority with which it took office in 2014. This certainly will have negative impact on stock prices.

That said, a lot of what is going on in the market right now is what can best be described as “herd mentality”, i.e. people getting influenced by each other and selling/ shorting the market based on the view that the current government will fall short of the majority mark.

The reality however is that even a slight deviation from the current and omnipresent view (of the government falling short of majority) will result in a sharp up move in stock prices. It is the same every election season. Traders bet on the outcome until the very last day and those with real news make a killing!

Elections aside, the historic (15 year) average price / earnings multiple for the Nifty is ~ 21. Up until the beginning of this week, this had shot up to 29. Put differently, stocks were 40% more expensive than their historic average. So elections and other factors put aside, frontline indices should fall at least 30% for stocks to become attractive (at least for a financial advisor). That said, Nifty or the Sensex do not really present the true picture.

So if your portfolio of mutual funds and mid/small cap stocks are not generating in line with broader markets, dont worry. This is line with how markets have performed. However, here’s what you should worry about – creating the right balance in your portfolio. First let’s understand why markets are on a tear.

There are 2 main reasons for this:

First, FII Buying & Selling

A look at what FII money has been doing since the beginning of this year will make things clear. Since the beginning of this year, FIIs have been constantly buying into Indian markets until the beginning of this month (i.e. May 2019).

Second, Mutual Fund Buying

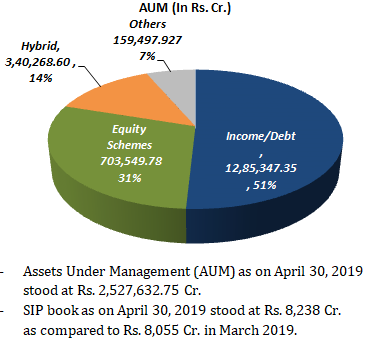

Unlike those who directly invest in stocks, Investors who started investing in the markets via SIP route do not get rattled easily. They do not monitor their investments frequently and hence these investments sustain. The amount of money getting invested in stock markets via SIP route stands at over Rs. 8,238 crore / month. The overall mutual fund industry’s AUM is close to Rs. 25.28 lakh crore. (To give you a perspective of how fast the industry has grown, the overall AUM touched Rs. 10 lakh crore for the first time in May 2014.)

For markets to fall in a big way, there must be some redemptions and stoppages of SIPs. Typically, when redemptions happen, they happen in bulk. This is when investors get spooked by a big market fall and stop their monthly commitments and redeem their existing holdings – this is when there is a dynamo effect. So far the fall has not been so sharp so as to spook domestic/ retail investors to redeem their holdings. On the contrary, both lumpsum and SIP investments into equity funds has been rising constantly over the past 2 years.

So What Can you do in these times?

Stick to (i) holding cash or (ii) fixed income funds or (iv) structured products where principal is protected (iv) Go short where you can risk it.

Within fixed income, I have a bias towards what is now widely considered as the riskiest class- Credit paper – these funds are facing incredibly difficult times. There are constant defaults and downgrades on corporate ratings because of which a lot of top rated corporate bonds and NCDs are trading below their face value.

Fear of defaults and redemption pressure has led to this price erosion despite 2 interest rate cuts in recent months. This, I believe presents the most compelling opportunity in this segment. I will not be surprised if many of these funds outperform their historic average and deliver a double digit return over a 24 – 36 month basis.

Naturally, going short always poses a risk of losing principal. If you must go short on specific stocks, make sure that you have sufficient margins to hold on to your short positions to ride out the current volatility. On a lighter note, a rather successful trader and a practitioner of the famous elliott wave theory recently told me he was convinced that Nifty will hit 12,000 over the next 1 month before it corrects. No matter what you do, keep this in mind and you will do just fine.

Disclosure: Currently holding substantial short positions on various client client accounts. I can be reached at rajat@sanasecurities.com | Comments below.

“Disclosure: Currently holding substantial short positions on various client client accounts.”

Have you turned from investment adviser to trader?

I thought, investment advisers are long only.

I am not sure what you mean. Going short was a 100% investment call. Not sure how others do it.

Your article need little correction – in last line it should read Nifty not sensex.

Thanks. Corrected 🙂