Updated on 27 December 2016

On 1 December 2016, Sunil Hitech issued 10:1 stock split and 1:1 bonus issue shares. For the purpose of this article, consider Sunil Hitech price as 20 times of its current market price.

If you have been reading my posts or of any other fundamental stock analyst, you would have noticed that typically they focus on 2 areas of research – qualitative & quantitative (i.e. financials).

Before I proceed, let me reiterate the importance of qualitative research i.e. that pertaining to quality and integrity of management, state of the industry, and future prospects of the business model.

Quantitative research deals with an analysis of financial data and accordingly the results are somewhat predictable. All future predictions here rely on a certain level of guess work about future growth, discount rates etc; most of which is based in part upon past growth. In other words, the idea is to look at past growth levels and adjust future growth a few notches up or down based on those levels.

Before you check the fair value of a stock on the basis below, keep in mind that:

- Past performance is no indicator of future results – Instead of using a standard growth rate or discount rate for future (based on past rates or otherwise), the better way to research is to anticipate future events and accordingly give growth predictions.

- No full proof system – There are many valuation techniques and those many improvisations made by analysts in their efforts to predict the future better than others. What you will find below is an easy to check the fair value of stock based on quantitative aspects.

_______________________

Fair Value Calculation

For the purpose of this example, I will take 2 stocks for my base calculations –

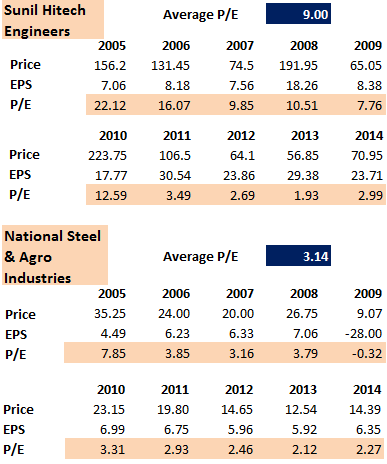

a) Sunil Hi-tech Engineering – we recommended this in our Multibagger portfolio on 18 November 2013 @ Rs 51 and exited from this stock on 2nd January 2014 @ Rs. 128; and

b) National Steel & Agro Industries – never recommended

Fair Value Based on Price Earnings (P/E) – It is easy to calculate the price earnings ratio of any stock by simply dividing its current price with its reported EPS of the last 4 quarters (take consolidated EPS). The best way to assess the PE is by comparing it to industry PE and with the historic PE of that specific stock.

At the current price of Rs 138 (as on 9 September 2014), Sunil Hi-Tech’s trailing 12 month PE comes to ~ 7.6 which is at a 15% discount to its 10 year average PE Multiple. It is another way of saying that the fair value of this stock should be Rs. 162 and you are getting it at Rs. 138. This is far below the industry PE (i.e. Power transmission and equipment; PE = 15).

At the current price of Rs 138 (as on 9 September 2014), Sunil Hi-Tech’s trailing 12 month PE comes to ~ 7.6 which is at a 15% discount to its 10 year average PE Multiple. It is another way of saying that the fair value of this stock should be Rs. 162 and you are getting it at Rs. 138. This is far below the industry PE (i.e. Power transmission and equipment; PE = 15).

At the current price of Rs. 24 (as on 9 September 2014), National Steel and Agro’s trailing 12 month PE comes to ~ 3.27 which is slightly higher than its 10 year average PE Multiple. However, it is far below the industry PE (i.e. Steel Sheets; PE = 20).

At these prices and based purely on PE analysis, Sunil Hi-Tech can be bought with a potential 15-25% year on year appreciation, with modest growth targets. For now, I would avoid buying into National Steel on these basis, unless there are any other strong external reasons to buy into this stock (which I may not be aware off).

Other factors affecting fair value of stock

That was a very basic (yet effective) way of arriving at some sort of fair value for a stock. There are many factors which may affect the fair value calculation. Future plans of the company, the general economic scenario, Industry specific news, are promoters buying or selling their holding?

To give you an example, MTNL stock has declined by nearly 90% over the last 6 years. With cellular service providers (like bharti Airtel, Vodafone and Reliance) gaining ground, was it justified to rely on the past financial performance and the wide pan-India reach of MTNL 6 years back? Go back a decade and it may be harder to answer this. At that time it seemed unreal that someone would eat into MTNL’s market share so quickly.

Also, you must define for yourself – the discount (in relation to fair value), at which you will be happy to buy a stock. 20 – 30 – 40%, i.e. your margin of safety or your margin for going wrong.

I have not word to praise for the way you have explained. Novice like me will take years to understand this but you made it so simple. Thank you very much. I love reading your every article. Thank you very much and please continue helping community to gain knowledge about investment.

It is most encouraging to get a praise from subscribers who had joined me when I had just started out. Thank you !

Thank u so much rajat for this wonderful article. We are blessed to be your blog followers.

Hoping even more wonderful writeups on stock valuation for beginners in stock market like me.

I know that valuation of stock is always subjective depending on our assumptions. But can you suggest me some good books to read on stock valuation which is real time based not theoretical and past trended.

Sure Geethanjali.

I compiled a list of my favorite books here – http://www.sanasecurities.com/best-finance-books-of-all-times , most of these are updated regularly based on current scenario. I recommend you read One up on Wall Street if you must choose 1 from the list.

I compiled some of my own blog posts, mainly the ones which were liked or commented upon the most and added by writing some more to make some E-books. You can get them here – http://www.sanasecurities.com/sana-securities-free-e-books

Very informative article. I always learn something new after reading your post.

Thanks Priyanka.

Not possible to get this type of Knowledge from other media. Thanks Rajat ji.keep it up.

Thanks a lot Satish.

Hi Rajat,

Hope that you are doing well.

Just wanted to point out that your calculation is SLIGHTLY flawed.

Take Sunil Hitech

You mention average PE is 9.

That is correct but incorrect as a measurement you need to used a weighted average which translates into 12.68 instead of 9.

The reasoning is simple that your PE has two components that are dependent on variable factors. Earnings are the residual of a P&L statement where so many other factors are at play. The stock price is a refelction of the player in the overall market.

So taking an average of PE is incorrect.

Using 12.68 (Add all the stock price/total of all Earnings) the discount is 39%.

Cheers

Varun

Why did the earnings go up from 2010 /2011 and the stock price go down? Stock splits and buyback?

I am good Varun. Thanks.

I wouldn’t say its flawed – just a little more practical. The idea of taking 10 year averages is to balance the numbers out. You may otherwise want to take the quarterly weighted average for the share price as well for it may be abnormally high on the day of our calculations. The only time I would want to do WA is when lets say there are a few years when the company reported a loss (i.e. negative EPS), that’s when the PE becomes zero for that year. For a 10 year average, that’s the only time I’ll think of WA.

But sure, go ahead and take WA, nothing wrong with that.

2010/ 2011 – Nope. All splits and buybacks are factored in. It was just bad for Indian markets in those years. Absolutely no logic to this!

This is the best explanations I have come across on the subject. Anybody who asks what is an ideal PE ratio should read this.

Thanks Rakesh.

Sir,

would you kindly say where can I get P/E of a stock for 10 yrs.period

Take the closing price of the stock for any given day. Divide that with total EPS of the previous 4 quarters, That is PE. When you do it for 10 years, take the price for the same day every year – like 31st March.

Is any of this your Stock of the month?

Not that I remember. If you are a subscribed member you can check here – http://sanasecurities.com/stock-analysis

Hello I tried this calculation a lot but from no where i landed up on a 23.95 eps for 2014 march sunil hitech fo rme it totalled at 20.55. Kindly elaborate the calculation for just the march 2014 part will do… If you can help me with syncom formulations (524470) same formula i ll be very grate ful to you.. Actually due to bonus the eps figures turn weird in the calculation.. Regards

How could you deduce the price of stock by calculating the PE.You didn’t mention that.

Not sure what to say. That’s the whole focus of the article.

Hi Rajat

First let me thx you pepole r doing grt hepl to us.

i m a new bee in to market not yet started trading but gathering knowledge before start. gone thru many video let me clear my english n maths both r very poor can u pl guide me any site which directly shows the fair price of the shares

or any kind of excel sheet which can go as per yr calculation.

THX IN ADV